HPE’s $14bn Acquisition of Juniper Networks

Written by: Dhivya Thangadhorai (Chapter President), Arnav Karode, Giulia Suhadinata, Alexander Bailey & Rishabh Madhok

Acquirer Overview: Hewlett Packard Enterprise (HPE)

Date Founded: 1 November 2015

CEO: Antonio Neri

Market Cap: $27.1 billion

LTM Revenue: $33.1 billion

LTM EBITDA: $3.8 billion

P/E: 23.8x

Ticker (NASDAQ): HPE

Deal Advisor: J.P. Morgan & Qatalyst Partners

History & Background

Hewlett Packard Enterprise (HPE) was formed following the corporate separation of Hewlett-Packard Company in November 2015, a strategic split that created two independent, publicly traded entities. Prior to the separation, HP had already begun strengthening its enterprise networking capabilities through the $3 billion acquisition of Aruba Networks in 2015, integrating Aruba’s wireless LAN and edge networking portfolio into what would become a core pillar of HPE’s future offerings. After the split, HP Inc. retained the personal systems and printing divisions, while HPE inherited the enterprise-focused businesses, marking the beginning of a renewed focus on hybrid IT and infrastructure solutions for large organisations. The newly formed company began trading on the NYSE under the ticker “HPE” in December 2015.

Since its inception, HPE has pursued a transformation strategy centred on high-margin, software-defined and cloud-enabled offerings. This has been driven in part by targeted acquisitions in the company’s formative years, including SGI, Nimble Storage and SimpliVity. These deals collectively repositioned HPE from a traditional hardware vendor to a modern, as-a-service infrastructure provider through its HPE GreenLake platform.

Product Lines

Hybrid Cloud: GreenLake is HPE’s flagship hybrid cloud platform that delivers compute, storage, networking, and software “as-a-service,” enabling organisations to run workloads on-premises, at the edge, or in the cloud with consumption-based pricing and unified management.

Networking: HPE delivers wired and wireless LAN, SD-WAN, and edge networking solutions primarily through Aruba Networks.

Storage & Data Management: Through products such as Alletra, Nimble Storage, and 3PAR, HPE provides cloud-native storage, disaster recovery, and intelligent data management solutions. These systems are optimised for hybrid cloud environments and integrate tightly with GreenLake.

Strengths

Prior to the acquisition, HPE held a strong financial position. Revenue for the first quarter of 2025 was $7.85 billion, marking a 16% increase from the previous year, reflecting high demand for AI systems.

Operating in over 170 countries, HPE has a strong global reach. A contributing factor for this is their global channel partner programme which allows them to deliver solutions to customers virtually.

HPE has a diversified product portfolio, strong in compute, storage, and networking. This reduces risk, provides more revenue opportunities and builds greater resilience against market volatility. GreenLake allows customers to use HPE technology on a pay-as-you-go basis, reflecting how HPE is working to meet the rising demand for hybrid-cloud infrastructure.

Challenges

HPE has faced several challenges leading up to the acquisition, one being margin pressure. Despite increased revenue in the first quarter of 2025, the non-GAAP gross margin declined by 680 basis points from the previous year. This was mainly due to the fall in server operating margin resulting from the high costs of AI chips. Between 2023 and 2024, revenue contracted by 9%.

Issues were also faced regarding its supply chain. HPE’s 2024 form 10-K outlines concerns surrounding component shortages, which had previously led to higher prices and delivery delays. There were also concerns regarding single-source suppliers, as any disruption with these suppliers would have large impacts on production.

Other challenges include the major operational change caused by integrating the HPE GreenLake platform, described on the 2024 10-K as “complex, costly and uncertain”.

Market Positioning

From a Porter’s Five Forces perspective:

Rivalry among existing competitors: HPE’s previous acquisition of Aruba allowed it to become a serious competitor to Cisco in WLAN. Other main rivals include Dell Technologies and IBM.

Threat of new entrants: Considered low risk due to high capital requirements for the enterprise IT infrastructure market. HPE also has an established brand and loyal customer base.

Threat of substitute products or services: Main threats are from public cloud providers such as AWS and Microsoft Azure, as well as competitors in IT infrastructure such as Dell Technologies and Cisco.

Bargaining power of buyers: Large enterprise clients have strong negotiating power; however, this is limited by HPE’s diverse customer base and the high costs of switching to competitors.

Bargaining power of suppliers: High, due to the limited availability of semiconductors, high demand for AI chips and the lack of supplier alternatives. HPE mitigates this through prioritising efficiency and sustainability in its operations.

Target Overview: Juniper Networks

History & Background

Juniper Networks was founded in 1996 in Sunnyvale, California, initially focusing on high-performance internet infrastructure for telecom operators and internet service providers. Its early breakthrough came with the M40 router, establishing Juniper as a credible challenger to Cisco, and created the foundation for its long-term position in global network infrastructure.

During the 2000s and 2010s, Juniper expanded from its original routing focus into enterprise networking, security, campus switching and data-centre solutions, including the acquisition of NetScreen Technologies in 2004. This diversification enabled Juniper to serve cloud operators, global enterprises and service providers with a product covering both core and edge requirements, and increased investment in software-defined networking and automation to support demand shifts towards cloud and hybrid architectures.

A major strategic inflection point occurred in 2019 with the acquisition of Mist Systems. Mist introduced a cloud-managed, AI- and machine-learning-driven networking platform that repositioned Juniper within the enterprise segment towards AI-operated and cloud-delivered networking. The acquisition increased the share of software and subscription-based revenue within Juniper’s portfolio, strengthening its presence in higher-growth and higher-margin segments.

Product Lines

Juniper’s product portfolio consists of several categories covering service-provider, cloud, and enterprise needs:

AI and Cloud Networking: The Mist AI platform provides a unified cloud-managed environment for wired networks, wireless networks and wide-area networks. This includes the Mist AI engine and the Marvis virtual assistant, which provides automated network operations, predictive analytics and self-healing capabilities. It offers centralised visibility, configuration automation, and predictive diagnostics, and represents Juniper’s strongest differentiator.

Routing: Juniper’s routing platforms includes the MX Series for multi-service edge environments, the PTX Series for packet transport and backbone networks, and the ACX Series for access and aggregation use cases including 5G. These systems are widely deployed by global telecom carriers and hyperscale operators.

Switching: The EX Series serves enterprise campus networks, and the QFX Series addresses datacentre switching and high-performance fabric designs. These switches are increasingly integrated with the Mist cloud and AI engine, allowing automated operations and improved visibility.

Wireless: Juniper’s wireless portfolio is built around Mist Wi-Fi, a cloud-native system that applies AI to deliver automated troubleshooting and real-time insights for enterprise wireless networks.

Security: The SRX family of firewalls supports datacentre and enterprise environments, and Connected Security extends security policies and analytics across the network fabric.

SD-WAN and Automation: Juniper offers cloud-delivered SD-WAN integrated with Mist, along with Paragon Automation tools used by service providers to manage wide-area and transport networks.

Strengths

Juniper Networks positions itself as a leader in AI networking and is recognised in the market for its innovation and operational excellence through its Mist AI platform.

Aside from its flagship product, the company’s remaining portfolio is strong and diversified, serving both small and large corporations. This is supported by consistently heavy R&D investment, e.g., $1.15bn in FY2024, reflecting Juniper’s long-term commitment to innovation.

Challenges and Market Positioning

The global networking industry is dominated by strong competitors, namely Cisco Systems, who occupy a 76% market share against Juniper’s 7% (2024), highlighting Juniper’s main weakness. Cisco remains one of the most dominant players in enterprise networking, with FY25 revenue of $56.7bn and strong gross margins of c.66%. Its continued scale in switching, routing, data-centre1 networking, and cloud-managed infrastructure means that any major shift in the competitive landscape, particularly in AI-driven networking, must be assessed in reference to Cisco’s position.

Motivations

HPE’s acquisition of Juniper Networks reflects a clear strategic push to reposition the company at the centre of AI-native networking. Primary motivations behind the deal include strengthening competitiveness, expanding into high-growth segments and improving long-term margin quality, and stem from HPE’s need to shift away from legacy hardware towards integrated, AI-driven infrastructure.

Cisco AI pivot forces HPE response: Cisco’s emerging strategy is to pivot towards “AI-native networking” in line with growing industry trends. The acquisition of Splunk, the company’s largest purchase in its history, and the unification of Meraki and Catalyst show how Cisco is reshaping its entire networking stack into a single AI-led ecosystem. Cisco’s strategic shift is reflected in increasing R&D investment annually, an area where HPE lacks. In 2024, HPE’s R&D spend was $2.246Bn, giving an R&D intensity of 7.46%, compared to Cisco’s 14.84%, a significant disparity suggesting insufficient R&D against industry benchmarks. In 2023, Juniper’s R&D intensity was a notable 21%.

Juniper products fill HPE automation gap: HPE’s long-term strategy is built around GreenLake as its core hybrid-cloud platform but requires improvements to compete effectively against hyperscalers and full-stack network vendors. The company does not have its own AI-driven networking platform, and developing such a product from scratch requires significant R&D, ongoing maintenance costs, and a highly specialised team, alongside commercial and execution risks given the fast-moving nature of the market and mounting pressure from competitors. Mist AI provides HPE with a leading cloud-management layer that improves network visibility and reduces operational complexity, directly supporting GreenLake’s value proposition of simplified, unified infrastructure oversight. Acquiring the already established MistAI technology provides an immediately implementable solution; Building these capabilities organically would otherwise take years, and still lack Juniper’s scale, intellectual property and brand strength. Junos OS, widely recognised for reliability and security, deepens HPE’s routing and security stack, enabling stronger integration across datacentre, campus, and edge environments.

Networking/software lifts HPE margins: HPE’s total gross profit margins are lower compared to industry peers, at 35.1% in FY23 and 32.8% in FY24, signalling a need to shift towards higher-margin recurring revenue. Juniper has maintained steady gross margins of roughly 58% in recent years, supported by service margins of ~71% and hardware margins of ~50%. Juniper notes in its 2024 press release that demand for MistAI and related cloud products grew >40% YoY following efforts to shift towards more scalable, subscription-based revenue. Market research expects demand to increase consistently going forward, with the enterprise networking market estimated to grow at CAGR of 5.4% between 2025 to 2030. Key acquisitions such as Nimble Storage and SimpliVity already signalled a long-term shift toward hybrid cloud, AI infrastructure, and intelligent data systems. Now, focusing on GreenLake, integrating MistAI delivers a complete platform rather than a collection of hardware-centric & higher-margin products, driving consumer stickiness and securing recurring revenue.

Talent acquisition: A secondary driver behind the deal is the opportunity for HPE to acquire Juniper’s specialised engineering and product talent, particularly in AI-driven networking, automation, silicon design and cloud-managed systems. Juniper employs thousands of engineers across its routing, switching and software divisions, including the teams behind the Mist AI engine. These capabilities have been critical to Juniper’s differentiation in automation, network assurance and AI-powered operations - areas where HPE historically lacked deep in-house expertise. Rami Rahim (former Juniper CEO) now leads HPE’s networking business (see Integration and Risks – Leadership Overview).

Deal Navigation

Financing Structure

The deal was an all-cash transaction valued at $14 billion, funded by a mix of HPE’s existing cash and new debt. Most of the financing came from committed term loan facilities, with the balance from cash and cash equivalents already on HPE’s balance sheet. Before the deal, HPE operated at a net debt-to-EBITDA ratio of 1.7, but this is expected to increase significantly to 3.0.

Moody’s reacted by placing HPE’s Baa2 ratings, while S&P500 gave a rating of BBB. This is largely due to the significant amount of debt being financed, resulting in increased leverage in the short term. Hence, this would place downward pressure on HPE’s credit rating.

HPE did not issue any new shares to fund the deal, and hence, there was no equity dilution, activist or proxy vote pressure for existing shareholders.

FY23 ($, bn)

Total debt = 12,355

CCE = 4,581

Net debt = 12,355 - 4,581 = 7,774

D&A = 2,616

Earnings from operations = 2,089

EBITDA = 2,616 + 2,089 = 4,705

Net debt/EBITDA = 1.7

Shareholder Return Targets

To support commitments to stronger free cash flow generation, HPE stated at deal announcement that the transaction is expected to be accretive to both non-GAAP EPS and FCF in the first full year post-close, supported by a higher-margin revenue mix and the integration of Juniper’s software-driven networking portfolio.

FY2026 guidance indicates $1.5-2.0 billion in FCF as integration benefits begin to materialise. HPE reaffirmed its intention to continue returning capital to shareholders through its dividend policy and potential share repurchases once the balance sheet stabilises. The company targets non-GAAP diluted EPS of at least $3.00 by FY2028, significantly above pre-deal levels and driven by recurring software, automation, and AI-native networking income streams. For more details, see Integration and Risks – Financial Integration Overview.

Regulatory Environment

From a regulatory perspective, the HPE–Juniper deal moved smoothly outside the US, with the EU, UK, and South Africa all giving unconditional approvals by mid‑2024. Shareholder approval at Juniper kept the deal on track, and it initially looked set to close on a normal timeline.

The US Department of Justice pushed back in January 2025, arguing that combining HPE and Juniper would leave just two major players controlling over 70% of the enterprise WLAN market. HPE initially argued that the DoJ’s definition of competition in the wireless-networking industry was too narrow but eventually addressed these concerns by divesting its Instant On WLAN business and licensing Juniper’s Mist AI source code to competitors. These actions ensured that the DOJ didn’t see the acquisition as anti-competitive and, following this, they cleared the way for the deal to close in early 2025.

Overall, the regulatory picture shows a clear split: outside the US, the merger wasn’t seen as a threat to competition, while within the US, targeted remedies ensured competition remained robust while allowing HPE to integrate Juniper’s capabilities.

Integration

Leadership Overview

Leadership alignment can be a decisive factor in the success of post-merger integrations, yet is often overlooked. It requires balance between strategic oversight, operational execution, and cultural alignment to ensure that the two companies synergise well, and significant challenges may arise from differences in decision-making style and risk appetite. In HPE’s case, the two leaders have a shared focus on AI and modernising enterprise IT, which is likely to drive a unifying strategic priority that ensures the successful alignment of the broader organisation.

Antonio Neri, CEO of HPE, has extensive experience across enterprise technology and has managed multiple complex acquisitions, including Aruba and Cray. His structured, strategic approach positions him well to effectively guide integration, allocate resources effectively, and protect the core business during this period of significant change.

Rami Rahim is the former CEO of Juniper and now spearheads HPE Networking. He offers deep technical and engineering expertise and a product-focused leadership style, which is essential for maintaining innovation and momentum in increasingly AI-driven networking products. Neri’s wealth of experience overseeing successful acquisitions, combined with his focus on enterprise-level strategy and market positioning, synergises with Rahim’s focus on technical execution, product development, and AI innovation.

Financial Integration Overview

HPE has outlined a structured financial integration plan for Juniper Networks, with value creation expected to emerge over the first three years following completion. At announcement, management approximated $450 million in annual run-rate cost synergies within 36 months, driven by procurement efficiencies, SG&A rationalisation and consolidation of overlapping corporate functions.

From a reporting perspective, the combined networking business is projected to account for roughly 31% of total revenue and over 50% of operating income on a pro forma basis. Juniper’s gross margins of approximately 58% at group level and over 70% for services are expected to lift HPE’s overall profitability as integration progresses. Integration-related cash outflows are anticipated to be concentrated in the first 12-18 months, before moderating as synergies are realised.

HPE has also linked the integration timeline to balance-sheet discipline, targeting net leverage of approximately 2x within two years post-close, supported by synergy capture and improving free cash flow. Overall, the integration strategy is expected to have attractive top-line and bottom-line growth opportunities both immediately and in the long term.

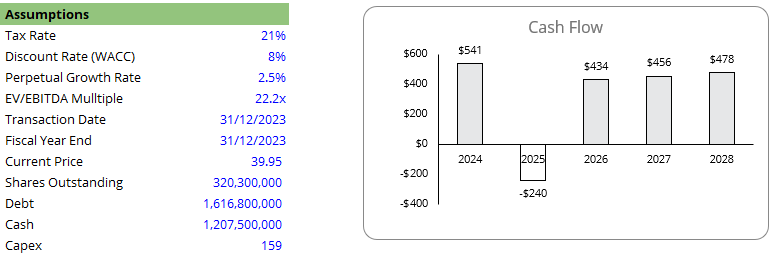

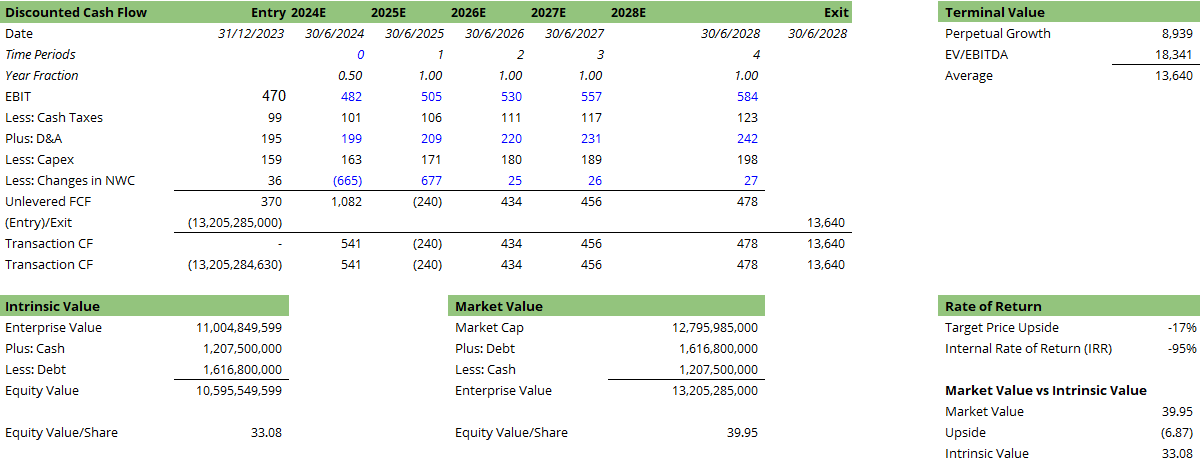

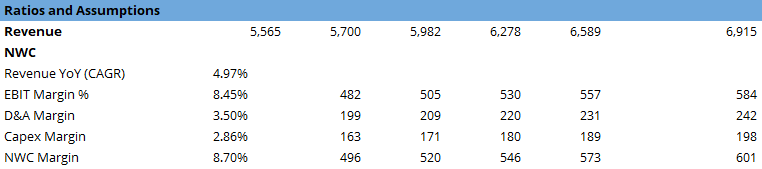

Valuation

Discounted Cash Flow (DCF) Analysis

Risks

Technological risk

Juniper’s technologies are built on cloud-native and data-driven approaches that differ from many of HPE’s existing networking and infrastructure solutions. The main challenge is not whether the technology works, but whether it can be integrated in a way that preserves its strengths without creating unnecessary complexity or slowing innovation.

Mist AI is one of Juniper’s most advanced offerings and relies on continuous data collection and machine learning to automate network management and improve performance. Integrating this into HPE’s wider portfolio, which includes Aruba networking as well as servers and edge systems, could be difficult. There is a risk that customers may face overlapping management tools or unclear workflows if Mist AI is not carefully aligned with HPE’s existing platforms. From a technical perspective, pushing Mist too quickly into a unified system could also reduce its flexibility and slow further development.

Juniper’s technology fits well with HPE’s focus on sustainability, but it presents its own set of challenges. Energy efficiency features are often closely linked to hardware design and firmware. This means Juniper’s power optimisation methods may not work consistently across HPE’s broad range of networking hardware. If some products benefit more than others, customers may see uneven results, which could weaken confidence in the overall platform.

For the integration to work smoothly, HPE will need to take a gradual and flexible approach. Allowing Juniper’s technologies to operate with a degree of independence in the short term would help maintain their performance and reliability. Over time, closer integration at the management and data levels could be introduced, provided it improves usability rather than adding complexity.

Several problem areas are likely to emerge during the integration process. Differences in engineering culture and development priorities could slow progress, as Juniper has invested heavily in cloud-based and AI-driven networking while parts of HPE still reflect more traditional enterprise infrastructure models. There is also the risk of customer uncertainty, particularly around product roadmaps and long-term support, which could affect trust if communication is unclear.

Overall, the technological risks involved in the HPE and Juniper acquisition are significant but manageable. Success will depend on how carefully HPE balances integration with preserving Juniper’s existing capabilities. If handled well, Juniper’s AI and energy efficiency technologies could strengthen HPE’s networking strategy. If handled poorly, they could become difficult to manage within an already complex product ecosystem.

Financial risk

The $14bn all-cash acquisition will significantly increase its leverage, increasing financial risk through higher debt servicing requirements and integration-related cash outflows. As a result, the combined group’s quality of earnings may decrease in the short run due to integration expenses. In addition, Juniper historically spends heavily on R&D, so even after integration, HPE will need to absorb this higher operating cost base. This could temporarily lower profit margins until synergies begin to materialise.

The incoming transition from hardware to software requires long-term implementation to lift margins. While the Mist AI product itself can be incorporated quickly, the impact on HPE’s margin profile will build gradually as more customers adopt Juniper’s software and cloud-managed services.

Juniper has exhibited relatively volatile revenue growth in recent years, with YOY growth from 11.9% in FY21 to 5.0% in FY22, followed by a decline of 8.8% in FY24, which increases the risk that earnings may underperform HPE’s expectations post-acquisition. This creates uncertainty around the timing and scale of synergy realisation and increases the risk that forecasted EBITDA would be overstated.

Furthermore, Juniper’s high net working capital requirements increase cash flow risk during integration. A high NWC indicates that more cash is tied up in current assets such as inventory and trade receivables, for day-to-day operations. HPE may need to commit additional cash to support inventory levels and trade receivables, which could place short-term pressure on its free cash flow. Together, these factors could constrain free cash flow and delay margin expansion until operational and cost synergies fully materialise.

Cultural risks:

Juniper operates with a strong engineering-led culture that is driven by innovation, such as its AI systems. On the other hand, HPE is much larger and more process-driven, with established structures implemented within the firm. This could lead to increased inefficiency and slower decision-making. In the long run, this may affect the retention of employees.

House View

HPE’s decision to acquire is strategically justified and well-timed and will materially strengthen HPE’s long-term competitive positioning in enterprise networking. The deal addresses the company’s existing structural weaknesses, i.e., the lack of AI-native networking and automation layers, margin pressures, and its R&D gap versus competitors.

The acquisition not only facilitates expansion but acts as defensive-offensive repositioning in response to Cisco’s accelerating AI-native strategy, whose growth requires competitors to guarantee platform stickiness and protect subscription revenues.

Technological integration risks remain material, particularly around preserving MistAI’s autonomy whilst avoiding overlap with Aruba and other HPE assets. However, given expert leadership & a ‘best-of-both’ approach to the merger, it is clear HPE is consciously avoiding over-integration. Financial risks are expected to be mitigated by the clear deleveraging path set out and the margin-accretive nature of the improved offerings.

If HPE executes the integration successfully, the transaction has the potential to reshape competitive dynamics by challenging Cisco on both innovation and architectural vision. Cisco is likely to respond by accelerating investment in AI-optimised hardware, deeper network-integrated security, and unified management platforms. As a result, the deal sets the stage for a more aggressive battle for share in next-generation enterprise networking.

References

https://www.hpe.com/us/en/about/history/timeline/timeline-growth-innovations.html

https://investors.hpe.com/financial/acquisitions

https://www.grandviewresearch.com/industry-analysis/enterprise-networking-market

https://www.spglobal.com/ratings/en/regulatory/article/-/view/sourceId/101633749

https://cbonds.com/news/2661371/

https://www.ansarada.com/article/mergers-acquisitions-integration-types