Weaker Yen, Stronger Policy Mix: Assessing Japan’s Economic Shift and Market Implications.

Japan's election of the spiritual successor to Shinzo Abe, Sanae Takaichi, marks a significant shift towards expansionary policies and a revival of Abecenomics.

A well-known advocate of Abenomics, Takachi’s political career has been filled with rhetoric signalling continuity with the late Shinzo Abe’s framework blending accommodative monetary settings with fiscal expansion and targeted structural reforms designed to lift Japan’s growth potential. As The Economist notes, she combines the “Thatcherite” image of economic discipline with a pragmatic tolerance for dovish monetary policy, last year remarking that the Bank of Japan would be “foolish to raise rates prematurely”.

How does the global macroeconomic outlook differ from that of when Abenomics was introduced on the global stage?

When Abenomics was introduced by Shinzo Abe in 2012, the global economy was united by weak growth and near-zero rates after the financial crisis, to tackle this the 3 arrows were implemented:

Quantitative easing through government spending and financial incentives (corporation tax was reduced from 35% to 29% from 2013 to 2018).

Ultra-loose monetary measures Implementing the Negative Interest Rate policy.

Corporate reform and workforce participation

Looking at Japan's economy today, and the picture has flipped:

Importantly, Japan hit the core inflation target of 2%, causing the BoJ to end its Negative Interest rate Policy in 2024 setting rates at 0.1% and raising it to 0.5% on June 17 2025.

Yet, as shown above, policy remains far looser than its peers with the Fed and BoE both seeing rates above 4% despite recent rate cuts.

Fiscal signs under Takachi point to further spending, despite other major economies tightening fiscal spending as global debt concerns loom in the forefront of policymakers’ minds.

Market Impact

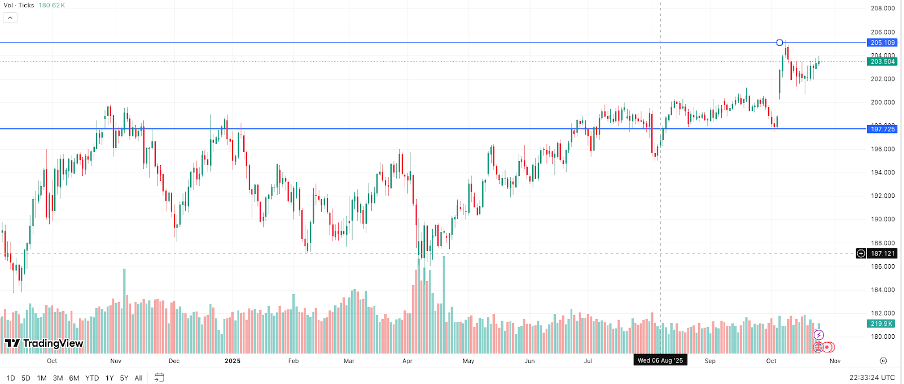

In a reaction to Sanae Takaichi's election, the GBPJPY rose from ¥147 to ¥152, signalling the market's strong expectations of expansionary fiscal policy and rate changes. Even with this weaker Yen, it still sits in the middle of its 3-year (¥140-¥160) and its calendar YTD range (¥145 –¥ 156). Despite the BoJ’s exit from negative rates, Japan’s yield remains among the lowest globally. This has continued to fuel carry trade activity, which is where investors borrow cheaply in yen to then fund higher-yielding assets abroad. A dynamic that has structurally weakened the currency in recent years.

Sanae Takaichi advocates highly for expansionary fiscal policy, so far she has put forward multiple tax cuts and subsidies while she is preparing a large economic stimulus package. While the exact number is unknown, it is highly likely that it will exceed last year's ¥13.9 trillion package. Most importantly, this boost in proposed spending combined with Japan's inflation still being above the BoJ target, is likely to accelerate the rate hike from 0.5 to 0.75, with an expectation for it to happen this quarter.

For investors, October 30 is going to be a day to watch. Historically the BoJ delays rate hikes when a new Prime Minister is elected and the markets have priced in a low chance of a rate hike. However, all economic factors point towards a rate hike and if they stay unchanged on Thursday then they are an almost certainty for December.

Market Outlook

Japan remains the most accommodative of the major economies, but with an adapting policy mix, the BoJ edges towards normalisation while the government maintains fiscal stimulus. Amid this dynamic, there are key market-moving events coming up that investors must be aware of:

The upcoming BoJ policy rate meeting and outlook report (Oct. 30) will be critical, with markets currently pricing a 40% chance of a rate hike before year-end. Potentially triggering a rally in the yen, which may test key support zones of USD/JPY and GBP/JPY.

In addition to this, an upcoming state visit (Oct. 27-29) from President Trump will likely move FX and equity markets, depending on the type of rhetoric coming out of either administration leading up to and following the visit.

Japan’s policy pivot sets up a mixed but opportunity-rich environment across asset classes. The yen is likely to remain structurally weak in the near term as fiscal expansion outpaces the Bank of Japan’s gradual tightening path. USD/JPY currently sits in the middle of its three-year range, and carry trades continue to thrive while global rate differentials remain wide. However, rising inflation pressures and elevated political focus on currency stability mean volatility and potential intervention risk will stay high heading into the BoJ meeting.

The BoJ meeting on the 30th October 2025, is critical, with markets currently pricing a 40% chance of a rate hike before year-end. Whether this takes place in the meeting in October or November, there will likely be a rally on the yen, which may test key support zones of USD/JPY and GBP/JPY.

Further, the state visit of President Trump on the 27th October 2025, will likely move FX markets, depending on the type of rhetoric coming out of either administration leading up to and following the visit.

Overall, Japan is transitioning from a deflation-scarred, yield-starved market into a credible reflation story. For investors, the backdrop supports an overweight to Japanese equities, ideally with selective FX hedging, and tactical positioning for yen volatility as policy moves become more data-driven and less predictable.

How can K2 help clients navigate this?

Bespoke FX services provided by K2, such as forward contracts, can help firms mitigate risk impacts on currency transfers with growing market uncertainty.

Providing expert advice to support clients in navigating this macroeconomic landscape, which is aligned with clients’ practical objectives and risk tolerance.

If you’d like to discuss these moves in more detail, or how they could impact your business or personal FX requirements, please don’t hesitate to get in touch.

How K2 FX Creates Value

Moving money across borders isn’t just a transaction, it’s a financial decision with real consequences. At K2 FX, we help you take control of currency risk by integrating FX strategy directly into your wider wealth picture. We provide:

FX forward contracts – secure today’s favourable rates for future payments, giving you certainty and peace of mind.

Automated rate targeting – use limit orders to capture upside without needing to watch the markets.

Proactive market intelligence – personalised monitoring and alerts, so opportunity never passes you by.

Clear, competitive pricing – institutional-level rates, no hidden charges, complete transparency.

Strategic alignment – we ensure transfers support your tax planning, investments, and long-term wealth goals.

When you’re transferring six or seven figures, even a 1–2% market move can mean tens of thousands gained or lost. Our clients trust us because we treat every transfer as a strategic moment, not an administrative task.

Disclaimer:

The information in this publication is provided for general information purposes only. It does not constitute financial or investment advice, nor should it be relied upon as such. Readers should consider their own circumstances and seek independent advice where appropriate.

Written by Jack Wilson (University of Nottingham). Edited by Jack Hurlford-Funnell & Bella Horvath