Service Now’s $7.75bn Acquisition of Armis

Written by: Aditi Prashanth (Chapter President), Dylan Dejahang, John Colman, Sampanna Raut & Vijay Karthikeyan

Deal Overview

Acquirer: Service Now

Target: Armis

Total Transaction Size: $7.75 billion

Announcement Date: December 14, 2025

On December 12th, 2025, ServiceNow (NYSE: NOW) entered into an agreement to acquire Armis for $7.75 billion in an all-cash deal. This is expected to be funded through a combination of cash on hand and debt and is expected to close in the second half of 2026. Armis was valued at $6.1 billion in a funding round on November 5th, 2025, which indicates the acquisition comes at a 27% premium.

This acquisition expands ServiceNow’s security offerings by adding Armis’ cyber exposure management, enabling end-to-end security action by connecting real-time asset discovery and risk prioritisation with automated remediation and response workflows. By linking Armis’ capabilities and dataset into ServiceNow’s AI Control Tower, ServiceNow strengthens trust, exposure management and identity governance, needed for secure AI adoption.

The market reaction to the leaked announcement that ServiceNow were in talks with Armis on December 14th, 2025, was negative. According to Bloomberg, the deal talk shock resulted in a fall from $173.01 (close: 12 Dec 2025) to $153.04 (close: 15th December 2025) or a 13% fall, which was amplified by a downgrade of ServiceNow to Underweight by KeyBanc. Commentary surrounding this fall was linked to ServiceNow potentially leaning on large, expensive inorganic growth, which raised concerns surrounding integration risk, overpaying and strategic drift.

Company Overview: Acquirer - ServiceNow

Founded: 2004

CEO: Bill McDermott

Market Cap: $153.1bn

LTM Revenue: $13.3bn

LTM EBITDA: $4.7bn

History & Background

ServiceNow evolved from a niche IT helpdesk utility (founded in 2004) into the dominant "Platform of Platforms" for the Global 2000. Following its 2012 IPO, the company displaced legacy incumbents by acting as a "System of Action" that integrates fragmented enterprise databases rather than replacing them. Under CEO Bill McDermott (appointed in 2019), ServiceNow expanded aggressively beyond IT into HR and Customer Service workflows, establishing itself as the core operational layer for digital transformation.

In 2025, the company pivoted its strategy toward "Agentic AI," deploying autonomous agents to execute complex cross-functional tasks without human intervention. This strategic shift, combined with disciplined "Rule of 50" growth and the acquisition of Armis to bolster security, has established ServiceNow as the definitive "AI Operating System" for the enterprise.

Product Lines

Technology Workflows - The company’s revenue engine, comprising IT Service Management (ITSM) and IT Operations Management (ITOM), provides total visibility into infrastructure and automates security responses (SecOps), serving as the critical foundation for the Armis acquisition.

Customer & Industry Workflows- A suite designed to compete with Salesforce by connecting front-office support directly to back-office operations. It includes vertical-specific solutions for Telecom and Finance that turn customer service from a cost centre into a proactive retention engine.

Employee Workflows- Anchored by HR Service Delivery (HRSD), this line provides a unified "Employee Centre" portal. It shields staff from backend complexity by handling onboarding, payroll and legal requests through a single consumer-grade interface.

Creator Workflows- Features the App Engine, a low-code development environment that allows non-technical "citizen developers" to build custom enterprise applications. This democratises innovation while keeping data within the secure governance of the Now Platform.

Strengths

High Stickiness & Switching Costs- ServiceNow acts as the "nervous system" connecting disparate enterprise applications, creating immense operational dependency. This deep integration drives a 98% renewal rate, as evidenced by major customers, like Siemens Healthineers, who use the platform to consolidate processes across hundreds of divisions.

Elite Financial Profile- Unlike most SaaS peers that sacrifice profitability for growth, ServiceNow consistently exceeds the "Rule of 50" benchmark. With approximately 21.5% subscription revenue growth and a 34% free cash flow margin (Q3 2025), the company generates the capital required to fund aggressive R&D and strategic M&A without diluting shareholder value.

Supply-Demand Advantage- The market demand for ServiceNow transformation is outpacing the supply of skilled talent. With demand for project services growing 55% YoY against a 43% growth in the talent pool, ServiceNow enjoys significant pricing power and leverage over its partner ecosystem (Accenture, Deloitte).

Challenges

Valuation Sensitivity - ServiceNow currently trades at a trailing P/E of ~93x and a forward P/E of ~37x, reflecting strong expectations of high growth relative to the current strength of earnings. With LTM EBITDA of ~ $4.7bn supporting $13.3bn of revenue, there is very limited tolerance for integration errors, as was reflected in the ~12% decrease in the share price following the Armis transaction.

Intensity of Competition - ServiceNow faces substantial competition from Atlassian, Microsoft, Salesforce, SAP and Oracle across business ITSM to workflow automation. The presence of these established incumbents increases pricing pressure, elongates deal cycles and forces heavy investment in R&D to maintain a competitive edge. Enterprise contracts are multi-year, driving high implementation costs with short-term pressure for ServiceNow.

Regulatory Lags - With ServiceNow’s operations being present in healthcare, the public sector and clients internationally, it’s subject to stringent data privacy, cloud compliance and cybersecurity regulations. The use of AI in workflows requires ServiceNow to assume greater legal responsibilities, and thus adhering to the array of regulations may result in constrained product development (due to high costs) and elongated business cycles.

Market Positioning

Business ITSM Leadership - ServiceNow, along with Atlassian, is globally recognised as a category leader in enterprise IT service management, establishing ServiceNow as a top-tier ITSM provider for the global 2000, allowing ServiceNow to benefit from long-term relationships and deep market penetration.

High Levels of Differentiation - The unification of multiple business functions under a single data model results in high switching costs and a unique selling point that siloed solutions struggle to replicate. This results in consumer stickiness, leading to predictable revenues from subscriptions. This is supportive for the long term, as it keeps customer acquisition costs contained.

Positioning within Risk Management and Security - Demand is shifting towards the option to connect workflows with greater protection, to optimise organisational response to threats. This trend is supported by the forecast that “worldwide end-user spending on information security and risk management will grow 12.5% in 2026, reaching nearly $240 billion,” allowing ServiceNow to compete for a growing share in the enterprise security market through the ability to embed its response into pre-existing workflows.

Summary

ServiceNow evolved from an ITSM provider founded in 2004 to an AI-driven workflow platform that spans IT operations, risk management, customer service and employee workflows following its 2012 IPO and repositioning under the strategic guidance of CEO Bill McDermott, now generating approximately $13.3bn in LTM revenue. Its platform model has driven adoption, with 98% renewal rates and substantial multi-year contracts that build upon its existing installed base.

The company serves organisations across both public and private spaces, trading at a strong valuation of ~93x trailing and ~37x forward earnings, reflecting strong growth expectations. Competing with a large number of incumbent firms, ranging from Atlassian to Microsoft, ServiceNow differentiates itself through its “nervous system” architecture, competing on depth and automation, while regulation and execution risks remain key considerations.

Company Overview: Target - Armis

Founded: 2015

CEO: Yevgeny Dibrov

Market Cap / Valuation (most recent valuation): $6.1 billion

ARR: $340 million

History and Background

Founded in 2015 by Israeli entrepreneurs Yevgeny Dibrov and Nadir Izrael, Armis addressed a critical cybersecurity gap: traditional locally-installed IT security tools could not identify or protect the rapidly expanding universe of IoT (Internet of Things) devices, operational technology systems, and medical equipment across enterprise networks (Armis, 2025). As cloud adoption accelerated, corporate attack surfaces expanded dramatically while visibility into these connected assets remained limited.

Armis developed an agentless, AI-driven platform that passively discovers devices through network traffic analysis, monitors behavioural patterns in real-time, and identifies vulnerabilities without requiring software installation on individual devices (ServiceNow, 2025). This approach proved essential in environments where traditional agent-based security was impractical, including medical devices in healthcare facilities, industrial control systems in manufacturing, and legacy operational technology in critical infrastructure (Armis, 2025).

The company's growth was driven by product innovation, strategic partnerships with enterprises in regulated industries, and successive venture capital rounds totaling $435 million in Series D funding at a $6.1 billion valuation in 2023, positioning Armis as a leader in cyber asset attack surface management (CAASM) (Calcalist, 2025). By 2025, Armis achieved $300 million ARR with customers across healthcare, financial services, manufacturing, energy, and government sectors (ServiceNow, 2025).

Product Lines

Armis offers a unified cloud-native security platform built around four core capabilities:

Asset discovery & management - Automatically identifies and inventories every device connected to enterprise networks, including IoT, OT, medical equipment, and unmanaged endpoints that traditional IT asset management systems fail to detect (Armis, 2025). This provides complete attack surface visibility across heterogeneous IT, cloud and operational technology environments (ServiceNow, 2025).

Security & threat detection - Continuously monitors device behaviour using machine learning to detect anomalies, malware, ransomware, and suspicious network activity in real-time (Armis, 2025). The platform establishes behavioural baselines and flags deviations indicating security incidents, complementing traditional perimeter and endpoint defences (ServiceNow, 2025).

Risk & compliance management - Assigns dynamic risk scores based on vulnerability assessments, network exposure and behavioural patterns (Armis, 2025). Armis supports compliance with HIPAA, PCI-DSS and NIST frameworks through continuous visibility and audit-ready reporting (ServiceNow, 2025).

Incident response automation - Integrates with SIEM (security information and event management) platforms and security operations tools to enable automated response workflows, including network segmentation, device quarantine and alert escalation, reducing mean time to respond (Armis, 2025; ServiceNow, 2025).

Strengths

Specialised expertise in emerging attack vectors - Armis leads the IoT and operational technology security market, a rapidly expanding segment that traditional cybersecurity vendors struggle to address effectively (TechTarget, 2025). With the global cybersecurity market expected to double by 2030, driven by AI adoption and connected device proliferation (CRN, 2025), Armis's deep domain expertise provides defensible differentiation in an increasingly crowded landscape.

Cloud-native architecture with agentless deployment - Built as a cloud-native SaaS platform, Armis scales efficiently and integrates seamlessly with modern enterprise stacks (Armis, 2025). Its agentless architecture monitors devices through passive network traffic analysis rather than requiring software installation, eliminating operational overhead and enabling security coverage for medical equipment, industrial controllers, and legacy systems that cannot support traditional agents (ServiceNow, 2025).

Proven track record in highly regulated industries - Armis has built strong customer relationships in healthcare, financial services, energy, and critical infrastructure, facing stringent compliance requirements (ServiceNow, 2025). These high-value, long-duration contracts create natural retention dynamics, as switching costs become prohibitively high once Armis is embedded in compliance workflows and security operations infrastructure.

Strategic complementarity with enterprise platforms - Unlike traditional cybersecurity vendors competing for IT budgets, Armis's asset visibility and threat detection capabilities complement enterprise workflow systems (Plat4mation, 2025). This positioning enables integration partnerships rather than competitive displacement, making Armis attractive for platforms expanding security capabilities without cannibalising existing products.

Strong financial performance and growth trajectory: With $300 million ARR growing over 50% year-over-year, Armis demonstrated clear product-market fit (ServiceNow, 2025). As a private, venture-backed company with no public debt, the acquisition structure simplified integration by avoiding debt assumptions or legacy liabilities (Calcalist, 2025).

Challenges

Competitive OT/ICS security landscape - Armis operates in a crowded OT and industrial security market alongside providers such as Claroty, Nozomi Networks, and Dragos. To remain competitive, Armis needs to keep differentiating on the quality of visibility, context, and response—rather than merely “finding devices”.

Broader exposure management competition - Beyond OT, Armis also competes within the wider exposure management space against established platforms such as Tenable, CrowdStrike, and Qualys, which increases pressure to demonstrate clear product superiority and ROI across enterprise buyers.

Remediation capability gap - Customers often note that while Armis’ detection and risk identification are strong, its remediation capabilities are comparatively weaker and require further development (David F., 2025). This creates execution and competitive risk, as rivals could close the detection gap while outperforming on “fixing the problem”, potentially weakening Armis’ differentiation over time.

Market Position

In terms of cyber-physical security systems, it has been ranked as a market leader alongside Claroty, Nozomi Networks, Dragos (and Microsoft) according to three separate sources: BankInfoSecurity, Industrial Cyber, and Omedia.

Financial Health

ARR surpassed $300m and referenced 50% growth in the company statement (Armis, 2025) - Reuters reported it raised $200m at $4.3bn (Oct 2025) valuation and raised $435m (Nov, 2025) at $6.1bn. This implies that the perceived value and financial health in terms of growth seem to be improving over time.

Summary

Armis is a cybersecurity company founded in 2015 that sells a cyber exposure management platform (Armis Centrix), providing real-time visibility across IT, OT and medical device environments. It positions itself around broad, agentless asset discovery and monitoring, with particular strength in cyber-physical and air-gapped settings, but faces heavy competition and some perceived weakness in remediation versus detection. In late 2025, it reported a $340m ARR and a $6.1bn valuation, and ServiceNow announced an agreement on 23 December 2025 to acquire Armis for $7.75 billion in cash (expected to close in H2 2026).

Motivations

For ServiceNow

Expansion into Security and Risk Management - Acquiring Armis improves ServiceNow’s security and risk management offerings, complementing its existing workflow platforms. Through this integration, ServiceNow advances its objective of reducing reliance on third-party security providers by providing end-to-end management of cyber exposures throughout an enterprise’s footprint.

Accelerated Time-to-market - Armis contributes a significant sum of $340m of ARR growing at over 50% YoY, with a proven track record in various industries. Replicating this internally would require multi-year development, improved execution risk and sustained R&D spending, considering that ServiceNow already spends 20% of its revenue on R&D to maintain a leadership position. By acquiring Armis, ServiceNow can immediately leverage the scalable platform, thus reducing the time-to-market.

Revenue and Diversification - The acquisition increases the risk profile in the regulated industries, thus significantly increasing the size of the addressable market available to ServiceNow. At the current time, in excess of 75% of subscription business comes from customers who have contracts in excess of $1 million in Annual Contract Value, which is indicative of the cross-selling opportunity. The acquisition further improves switching costs, contracts, and subscription revenue.

For Armis

Overcoming Scaling Constraints - Since its founding in 2015, Armis scaled as a specialist cyber exposure management firm, but faced structural restrictions when competing against multi-product platforms with global distribution. Through integration with ServiceNow, Armis has instant access to an established salesforce and customer base, improving scalability and reach.

Operational synergies - Armis’ agentless platform monitors billions of connected assets across different business environments, delivering strong risk assessments; however, relying on third-party remediation tools. Through embedding its services with ServiceNow, Amris’ product is elevated from a monitoring tool to a core operational capability, as ServiceNow’s workflow structure now enables automated response and execution.

Strategic Timing in a Consolidating Market - Following Armis’ acquisition by Insight Partners in 2020, initial rapid expansion was seen to face increasing marginalisation risk as cybersecurity consolidated across integrated platforms. Armis can achieve long-term financial sustainability, relevancy and sustained innovation through the acquisition by ServiceNow.

Deal Navigation

Regulatory & Legal

The main regulatory & legal risks can be separated into multiple different sub-categories. The first includes competition and antitrust risk. This acquisition would be considered a conglomerate acquisition. This is because Armis and ServiceNow are not competitors and do not share suppliers in the same value chain, but offer complementary products which might be bought by the same consumers. In the UK, according to the CMA, an investigation would take place provided that their annual turnover in the UK exceeds £100 million or the conditions for 2.2(b)(i)-(iii) are met on the CMA’s ‘Quick Guide to UK Merger Assessment’ report. According to the CMA, if this merger results in a realistic prospect of a lessening of competition (SLC), then it might pursue an investigation. In the context of ServiceNow, the acquisition of Armis might result in an investigation if there is evidence to suggest that the merged business has the ability and incentive to harm overall competition in the UK cybersecurity market (see paragraphs 3.16-3.17).

One strategy could involve ServiceNow offering Armis’s services at a lower price through bundling it with the Now Platform. ServiceNow does not indicate whether it will use harmful strategies to reduce overall competition, so the outcome is unknown, although the conditions to meet 2.2(a) and 2.2(b)(i)-(iii) regarding CMA investigating this acquisition in the first place is unlikely to be met.

In the US, antitrust and regulatory risk are more material. Since the deal is valued at approximately $7.75 billion, it exceeds the HSR size-of-transaction threshold ($133.9m for 2026) and also exceeds the $535.5m level at which the size-of-person test does not apply. Therefore, absent an exemption, the parties would need to file HSR premerger notifications with the FTC and DOJ and observe the waiting period before closing (30 days after complete filing).

This creates timing and closing risk, as the transaction cannot be completed until the HSR waiting period has expired, and the DOJ or FTC can issue a “second request”, which can extend the timeline and lead to business disruption. In addition, this transaction falls within the top HSR filing-fee tier, meaning ServiceNow will face a filing fee of $2.46 million, although this is immaterial relative to the total transaction value. The transaction could also be blocked altogether if there is evidence to suggest it would substantially lessen competition. Finally, an investigation creates remedy risk, where clearance may require divestitures, limits on bundling, or other commitments that could materially affect the value ServiceNow attaches to the deal.

Armis’s and ServiceNow’s operations extend across multiple jurisdictions, which implies that, to comply with multiple local laws, ServiceNow may need to incur significant legal costs and faces a risk of non-compliance.

Financing Structure

As mentioned earlier, ServiceNow will acquire Armis for $7.75 billion. According to ServiceNow, the deal will be all-cash, subject to customary adjustments. This amount will be funded both through cash-on-hand and debt, with no equity consideration. The deal is anticipated to be completed at the close of H2 2026, subject to regulatory approvals and customary timings. The advisors on this deal include Tidal Partners (lead), with JP Morgan and Barclays also advising ServiceNow. Armis is to have stated that its ARR is above $340 million, which implies that the purchase price is approximately 22.8x ARR.

Integration

Culture and Talent

ServiceNow operates a process-oriented and centralised enterprise platform, whereas Armis is a dynamic, specialist cybersecurity firm. This difference in cultures heightens risk in terms of decision-making speed and autonomous products. Retention of key Armis engineers is critical, as substantial deal value lies in human capital and proprietary IP.

Technical Risks

An important execution challenge is the integration of real-time device intelligence with ServiceNow’s workflow automation, CMDB, and AI Control Tower. Delays in this process could lead to confusion and limit revenue synergies in the short term.. Poor execution would result in a coupled product rather than a platform extension.

Operational Implications

Initial duplicated systems, long development cycles and incremental cloud spend may increase operational costs. If the development cycles stretch out, the benefits to be achieved by improving operational efficiencies and the ability to leverage the power of cross-selling may be delayed. ServiceNow’s phased integration approach mitigates disruption at the cost of higher pressure on medium-term execution discipline.

Performance and Valuation

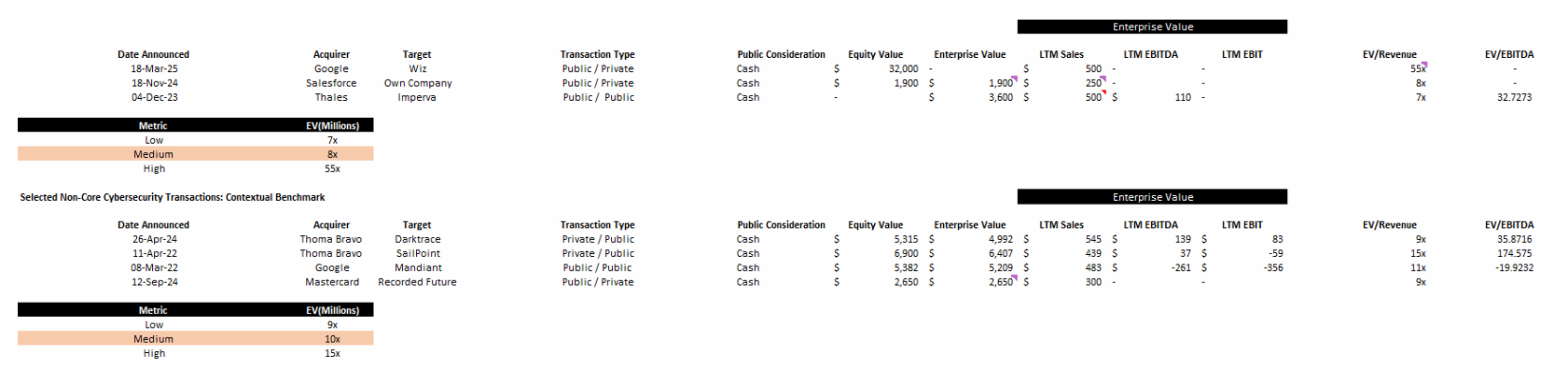

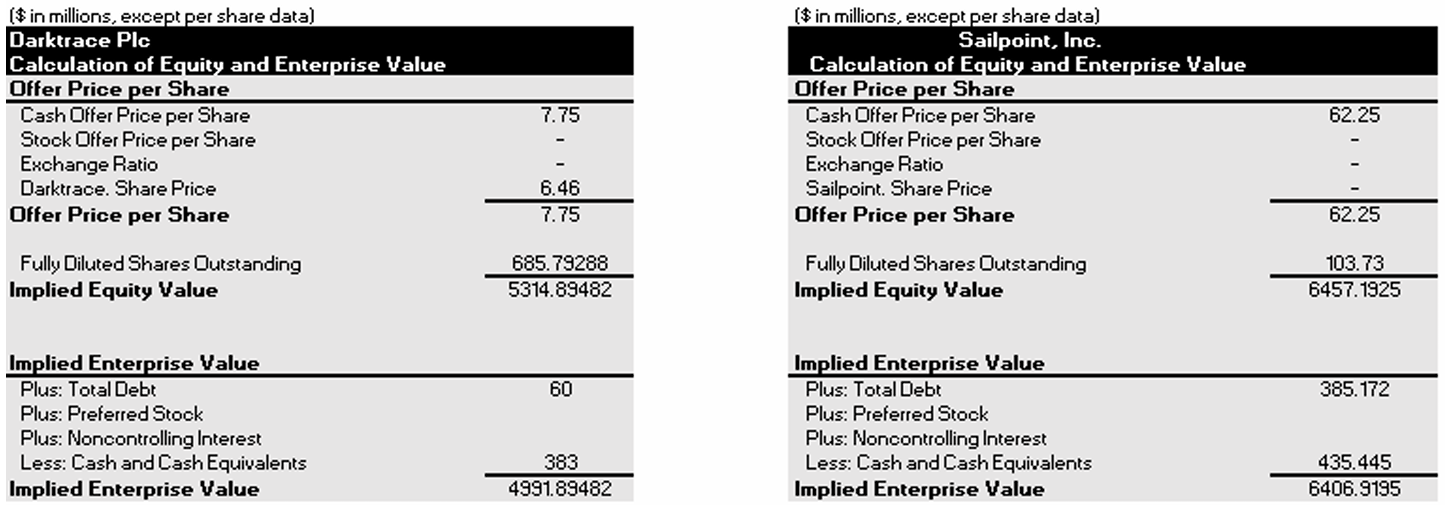

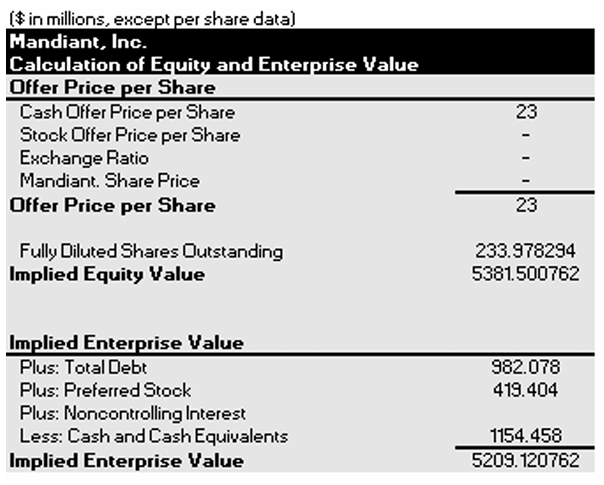

Precedent Transaction Analysis

Using Armis’s annual recurring revenue (ARR) as a proxy for LTM sales and its purchase price of US$7.75 billion as a proxy for its EV, we can assume ServiceNow acquired Armis at an EV/Revenue multiple of 22.8x. This sits towards the upper end of the range for core and non-core cybersecurity transactions, implying that ServiceNow has more optimistic forward expectations about the value the deal will create, driven by anticipated synergies.

Furthermore, over the past two years, three significant transactions have taken place in which direct and close competitors have acquired cybersecurity companies, which may have strengthened sellers’ negotiating leverage and materially pushed up the price to a higher LTM multiple.

Using Armis’s annual recurring revenue (ARR) as a proxy for LTM sales and its purchase price of US$7.75 billion as a proxy for its EV, we can assume ServiceNow acquired Armis at an EV/Revenue multiple of 22.8x. This sits towards the upper end of the range for core and non-core cybersecurity transactions, implying that ServiceNow has more optimistic forward expectations about the value the deal will create, driven by anticipated synergies.

Furthermore, over the past two years, three significant transactions have taken place in which direct and close competitors have acquired cybersecurity companies, which may have strengthened sellers’ negotiating leverage and materially pushed up the price to a higher LTM multiple.

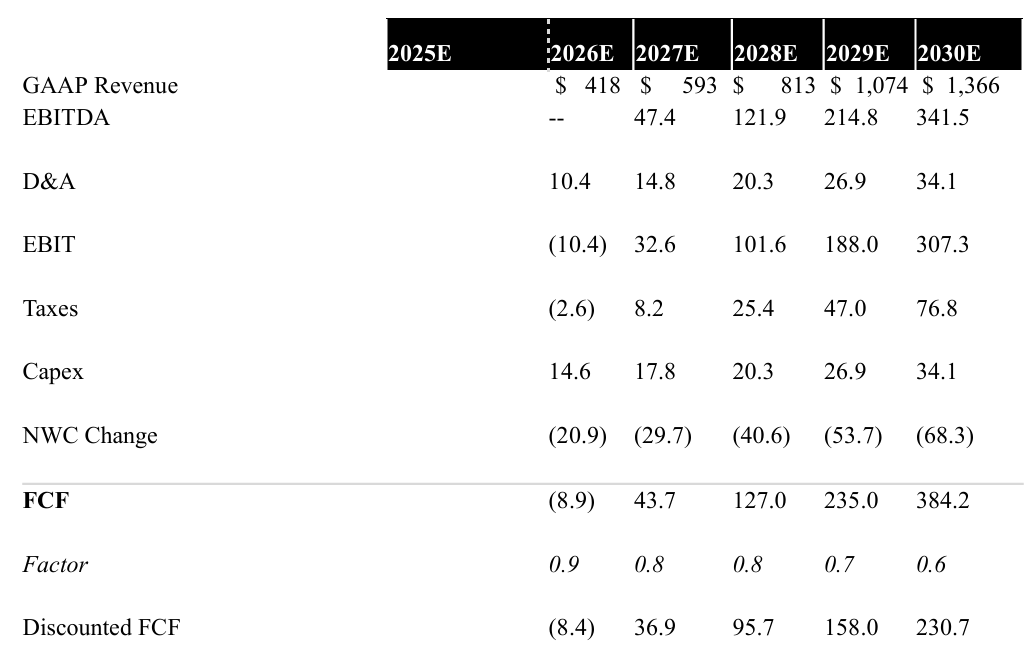

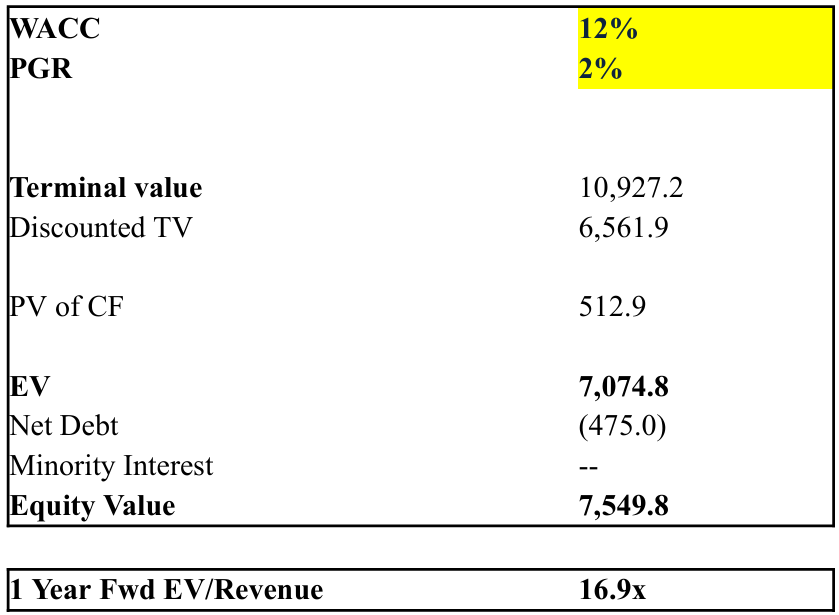

Discounted Cash Flow Analysis

Our speculative calculation implies an equity value per share totaling $7,549.8 million, within an approximate 3% deviation from ServiceNow’s current price tag of $7.75 billion. This clearly indicates that the deal is driven by thoroughly rational inherent valuations, thus negating any idea of premium pricing, making any post-deal synergies additional upside for ServiceNow.

The question, however, is that this should not be overstated. The matching statistic, while dependent upon outside information rather than inside data, should also not be taken as being definitive. Given that the valuation is so sensitive to unnatural growth assumptions, this can only act as validation for the logic of the deal itself.

Risks

UK and international regulatory risk

The deal is best viewed as a conglomerate acquisition (complementary products rather than direct competition), so the principal UK risk is CMA scrutiny if jurisdictional thresholds are met (e.g., UK turnover > £100m or the 2.2(b)(i)–(iii) conditions) and the CMA identifies a realistic prospect of an SLC. Any review would likely focus on whether ServiceNow could use bundling (e.g., integrating Armis with the Now Platform) to foreclose rivals in UK cybersecurity markets, creating potential remedy risk (behavioural commitments) and added cost and complexity from multi-jurisdiction compliance.

US antitrust and closing risk (HSR)

US risk is more material because the ~$7.75bn consideration exceeds the HSR size-of-transaction threshold ($133.9m for 2026) and the $535.5m level where the size-of-person test does not apply, so (absent an exemption) HSR filings with the FTC/DOJ and the waiting period are required before closing. This introduces timing and execution risk, particularly if a “second request” extends the timetable and disrupts operations, and it also creates remedy/block risk if the agencies conclude the transaction would substantially lessen competition, even though the top-tier HSR filing fee (~$2.46m) is immaterial to deal value.

House View

Viewpoint

The ServiceNow-Armis acquisition has a strong strategic rationale; however, the execution bar is high, and it forms part of a broader trend of ServiceNow relying more heavily on inorganic growth. The EV/ARR is approximately 22.8x, which is higher than both non-core and core deals in our PTA analysis. For this deal to justify its elevated valuation, Armis must sustain over 50% growth, its products must be effectively cross-sold, and the platform integration must be delivered successfully. Moreover, recent large acquisitions, particularly in the AI space (e.g., Element AI and G2K), suggest ServiceNow is accelerating its M&A activity in response to the AI boom. Overall, my view is mixed: Armis offers clear strategic logic, but the demanding execution requirements make this a higher-risk transaction given the price paid.

Positive Signals

Balance-sheet capacity and funding flexibility - balance-sheet headroom supports an all-cash deal without stretching leverage or materially weakening interest cover. Leverage has de-risked meaningfully from 2021 to 2024 (EBITDA leverage: 2.03x to 0.77x; capitalisation: 28.7% to 13.4%; interest cover: 17.8x to 83.8x). Furthermore, liquidity can fund a substantial portion of the purchase price, reducing reliance on new borrowing and debt-market conditions.

Strong strategic fit within a scaled go-to-market engine - ServiceNow’s Security & Risk business has surpassed $1bn ACV (3Q25) and has an established go-to-market engine, whilst Armis brings a fast-growing (>50% YoY) ARR base and expands coverage across OT, IoT and medical devices. This combination supports a clear value-creation path via cross-sell and a higher recurring revenue mix.

Structural tailwinds and value-creation pathway - the deal fits the AI-driven “expanding attack surface” theme and strengthens demand for automated remediation. Furthermore, the acquisition is positioned as product and growth-led rather than purely financial, improving the odds of earning its cost of capital.

Emerging Risks

Physical World Liability - The shift to "Agentic AI" takes ServiceNow from ticketing IT into industrial system control. With this comes the ability for automated errors impacting physical critical infrastructure, like pipeline and ventilator systems, to invoke unprecedented physical liability claims, as any of the existing EULAs will probably not address.

The "Suite Trap" - The integration of Armis risks alienating CISOs who favour "best-of-breed" agility over platform bundles. If the combined offering is perceived as bloated architectural debt rather than seamless value, ServiceNow faces churn among elite customers refusing to trade specialisation for a "jack-of-all-trades" ecosystem.

Forward Insight

As ServiceNow is saturated in IT Service Management, ServiceNow needs a new growth engine to sustain its ~37x P/E multiple, which is a survival play to "rent" Armis’s growth storyline at a premium to access the $240bn security TAM. ServiceNow without Armis faces potentially dangerous “Data Blindness.” This deal assures them of attaining the necessary “Visibility” in an IoT/OT world so they can stay ahead of their competition in the Industrial AI race.

References

Alcor Solutions, Inc. (2025) ‘Top ServiceNow trends 2025: AI leads the way in next-gen business transformation’. Available at: https://www.alcorsolutions.com (Accessed: 30 January 2026).

Alphabet Inc. (2025) ‘Current report on Form 8-K (Wiz transaction’), U.S. Securities and Exchange Commission, 18 March. Available at: https://www.sec.gov/Archives/edgar/data/1652044/000165204425000027/goog-20250318.htm (Accessed: 9 January 2026).

Amazon Web Services (2025) ‘Armis device security platform reviews’. Available at: https://aws.amazon.com (Accessed: 30 January 2026).

Armis (2020) ‘Insight Partners to acquire Armis for $1.1 billion valuation’, Armis Blog, 6 January. Available at: https://www.armis.com/blog/insight-partners-to-acquire-armis-for-1-1-billion-valuation/ (Accessed: 30 January 2026).

Armis (2023) ‘Armis becomes fastest-growing cyber start-up, reaching $100m ARR in under five years’, Press release. Available at: https://www.armis.com/newsroom/press/armis-becomes-fastest-growing-cyber-start-up-for-asset-visibility-intelligence-security-reaching-100m-usd-arr-in-less-than-5-years/ (Accessed: 30 January 2026).

Armis (2024a) ‘Armis raises $200m at $4.2bn valuation as growth soars’, Press release, 28 October. Available at: https://www.armis.com/newsroom/press/armis-raises-200m-at-4-2b-valuation-as-growth-soars-eyes-ipo/ (Accessed: 30 January 2026).

Armis (2024b) ‘Armis surpasses $200m ARR, doubling ARR in under 18 months’, Press release. Available at: https://www.armis.com/blog/200m-arr-milestone-nadir/ (Accessed: 30 January 2026).

Armis (2025a) ‘Cybersecurity leader Armis closes $435m funding round at $6.1bn valuation’, Press release, 5 November. Available at: https://www.armis.com/newsroom/press/cybersecurity-leader-armis-raises-435-million-round-at-6-1-billion-valuation/ (Accessed: 30 January 2026).

Armis (2025b) ‘Armis surpasses $300m annual recurring revenue’, Press release. Available at: https://www.armis.com/newsroom/press/armis-surpasses-300m-arr-as-demand-for-exposure-management-security-soars/ (Accessed: 30 January 2026).

Armis (2025c) Armis platform overview. Available at: https://media.armis.com/pdfs/br-armis-overview-en.pdf (Accessed: 8 January 2026).

Armis (n.d.) Armis Centrix™ platform. Available at: https://www.armis.com (Accessed: 30 January 2026).

BankInfoSecurity (2025) ‘Claroty, Nozomi and Armis top cyber-physical security rankings’, BankInfoSecurity, 28 February. Available at: https://www.bankinfosecurity.com (Accessed: 30 January 2026).

Bloomberg (2025) ‘ServiceNow is said to near up to $7bn deal for Armis’ (video), 15 December. Available at: https://www.bloomberg.com (Accessed: 1 January 2026).

Calcalist (2025) ‘Armis acquisition marks largest Israeli cybersecurity exit’, Calcalist, 23 December. Available at: https://www.calcalistech.com/ctechnews/article/dxlu0k10s (Accessed: 8 January 2026).

CompaniesMarketCap (n.d.) ‘ServiceNow market capitalisation’. Available at: https://companiesmarketcap.com/servicenow/marketcap/ (Accessed: 1 January 2026).

CRN (2025) ‘ServiceNow to acquire Armis in $7.75bn all-cash deal’, CRN, 23 December. Available at: https://www.crn.com/news/security/2025/servicenow-to-acquire-exposure-management-vendor-armis-in-7-75b-all-cash-deal (Accessed: 8 January 2026).

Darktrace plc (2023) Final results, RNS announcement, 6 September. Available at: https://www.investegate.co.uk (Accessed: 9 January 2026).

Forrester Research (2023) The Forrester Wave™: IT service management platforms, Q4 2023. Available at: https://www.forrester.com (Accessed: 1 January 2026).

Gartner (2025) ‘Gartner forecasts worldwide end-user spending on information security and risk management to reach $240bn in 2026’, Press release, 29 July. Available at: https://www.gartner.com (Accessed: 1 January 2026).

G2 (2025) ‘Armis review by David F.’, G2, 29 October. Available at: https://www.g2.com/products/armis/reviews/armis-review-7138113 (Accessed: 1 January 2026).

Globes (2023) ‘Thales acquires Imperva for $3.6bn’, Globes. Available at: https://en.globes.co.il (Accessed: 9 January 2026).

Industrial Cyber (2023) ‘Armis, Nozomi, OTORIO and Dragos named leaders in GigaOm Radar’, Industrial Cyber, 10 July. Available at: https://industrialcyber.co (Accessed: 30 January 2026).

Industrial Cyber (2025) ‘Armis secures $435m pre-IPO funding, valuation hits $6.1bn’, Industrial Cyber. Available at: https://industrialcyber.co (Accessed: 30 January 2026).

Insight Partners (2020) ‘Insight Partners acquires Armis at $1.1bn valuation’, Press release, 6 January. Available at: https://www.insightpartners.com (Accessed: 30 January 2026).

Investing.com (n.d.) ‘ServiceNow Inc. historical data’. Available at: https://uk.investing.com (Accessed: 1 January 2026).

KeyBanc Capital Markets (2024) KBCM technology group SaaS survey. Available at: https://info.sapphireventures.com (Accessed: 30 January 2026).

Macrotrends (n.d.) ‘ServiceNow EBITDA 2012–2024’. Available at: https://www.macrotrends.net (Accessed: 1 January 2026).

MarketWatch (2025) ‘ServiceNow to buy Armis for $7.75bn’, MarketWatch, 23 December. Available at: https://www.marketwatch.com (Accessed: 1 January 2026).

Omdia (2022) ‘Armis leads OT security market amid intensifying competition’, Omdia, 23 March. Available at: https://omdia.tech.informa.com (Accessed: 1 January 2026).

Omdia (2025) Omdia Market Radar: OT cybersecurity platforms 2025. Available at: https://omdia.tech.informa.com (Accessed: 1 January 2026).

PitchBook (2026) Armis company profile: valuation, funding & investors. Available at: https://pitchbook.com (Accessed: 30 January 2026).

Reuters (2024) ‘Cyber firm Armis raises $200m at $4.3bn valuation’, Reuters, 28 October. Available at: https://www.reuters.com (Accessed: 30 January 2026).

Reuters (2025) ‘Cybersecurity firm Armis valued at $6.1bn in latest funding round’, Reuters, 5 November. Available at: https://www.reuters.com (Accessed: 1 January 2026).

Sacra (2025) Armis: revenue, funding and business model analysis. Available at: https://sacra.com (Accessed: 30 January 2026).

ServiceNow, Inc. (2019) Siemens customer case study. Available at: https://www.featuredcustomers.com (Accessed: 30 January 2026).

ServiceNow, Inc. (2025) Form 10-K (FY ended 31 December 2024). U.S. Securities and Exchange Commission. Available at: https://www.sec.gov (Accessed: 1 January 2026).

ServiceNow, Inc. (2025) ‘ServiceNow to acquire Armis to expand cyber exposure and security’, Press release, 23 December. Available at: https://investor.servicenow.com (Accessed: 9 January 2026).

StockAnalysis (n.d.) ‘ServiceNow stock price history’. Available at: https://stockanalysis.com (Accessed: 1 January 2026).

TechTarget (2025) ‘ServiceNow: definition and overview’, SearchITOperations. Available at: https://www.techtarget.com (Accessed: 8 January 2026).

Thales (2023) ‘Thales to acquire Imperva’, Press release, 25 July. Available at: https://www.thalesgroup.com (Accessed: 9 January 2026).

Thoma Bravo (2022) ‘SailPoint to be acquired for $6.9bn’, Press release, 11 April. Available at: https://www.thomabravo.com (Accessed: 9 January 2026).

Thoma Bravo (2024) ‘Completion of Darktrace acquisition’, Press release, 1 October. Available at: https://www.thomabravo.com (Accessed: 9 January 2026).

Yahoo Finance (n.d.) ‘ServiceNow historical data’. Available at: https://uk.finance.yahoo.com (Accessed: 1 January 2026).