The Physical Cost of AI: A Structural Decoupling for the Chilean Peso and Peruvian Sol

The Peruvian Sol (PEN) and the Chilean Peso (CLP) present a compelling setup for observation. Market factors currently signal that certain countries in the Andean foreign exchange block of South America might separate from the others over the following months. The massive power infrastructure required for Artificial Intelligence (AI) points toward a sustained demand for copper. Because copper accounts for roughly 57% of Chile's total exports and over 30% of Peru's total exports, the current AI infrastructure trends could position the Chilean and Peruvian currencies as highly resilient assets. However, market regimes remain fluid, and these outcomes are not guaranteed.The architectural shift in technology is driving these market signals right now. Companies are transitioning from traditional data centers, which use 5 to 10 megawatts of power, to massive AI facilities that demand up to 30 megawatts per individual workload. The new AI facilities run extremely hot. To prevent the computer servers from overheating, the new facilities require advanced liquid cooling systems and heavy electrical wiring. Those specific cooling and wiring systems require up to 47 metric tons of copper per megawatt, nearly double the amount used in older air-cooled facilities. Simultaneously, mining companies have slashed early-stage exploration budgets to just 28% of total spending. If current trends continue, the lack of mining exploration suggests the global market might face a severe copper supply shortage of over 150,000 metric tons by the end of 2026. Consequently, global capital could rotate into Chile and Peru to secure existing copper output.The copper supply signals suggest a potentially positive outlook for the Chilean Peso and the Peruvian Sol. Central banks generally face a big limitation: the zero lower bound over the nominal interest rate. Another major limitation is the possibility of inflation if a decrease in the interest rate is not controlled carefully. To target that inflation risk, one standard tool is fiscal policy. However, Chile and Peru might not need drastic fiscal changes. Peru currently boasts a massive 2.3% current account surplus, while Chile maintains a highly manageable 42.6% debt-to-GDP ratio backed by strong foreign direct investment. Those financial cushions might allow the Peruvian and Chilean central banks to safely hold interest rates steady (around 4.25% and 4.50%, respectively). In contrast, countries like Brazil currently face a staggering 95% debt-to-GDP ratio and a punishing 15% interest rate. If the current trajectory holds, investors might bet against the burdened Mexican and Brazilian currencies to fund investments in the stronger Andean markets.Because macroeconomic conditions constantly evolve, our upcoming research will track several specific variables to test the current framework. First, we will monitor the computer chip supply chain. If technology companies experience AI chip shortages, those companies might delay building new data centers. A delay would temporarily reduce the projected 165% growth in data center power demand by 2030. Second, we will track copper storage levels in the United States. Supply chain hoarding ahead of potential new trade tariffs can make global copper inventories look artificially high. Finally, we will watch the political environments in Mexico and Brazil. For instance, if the Brazilian government unexpectedly implements strict laws to resolve Brazil's 95% debt-to-GDP issue, the Brazilian Real could strengthen rapidly and invalidate the short side of the proposed trade.Macro Regime

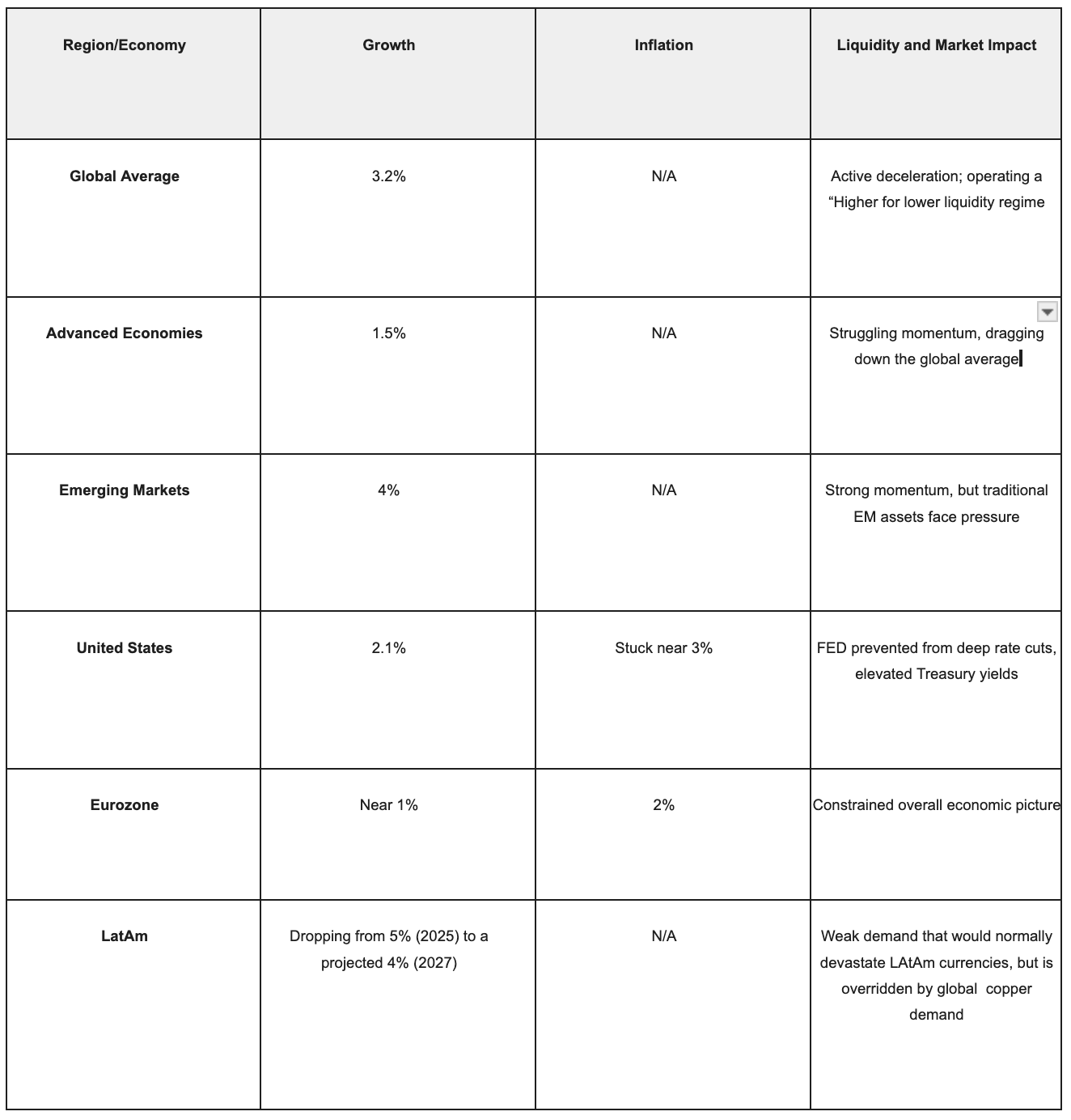

1. Growth, Inflation, and Liquidity ConstraintsThe global economy in March 2026 operates under a “Higher for Longer” liquidity regime. Global macroeconomic growth is actively decelerating. The International Monetary Fund projects global expansion will slow to 3.1% in 2026. That 3.1% figure represents a measurable drop from 3.2% in 2025 and 3.3% in 2024.That headline growth number hides a massive performance gap between different global regions. Advanced economies are currently struggling, showing only 1.5% average growth. Meanwhile, emerging market economies maintain strong momentum, sustaining aggregate growth rates near 4.0%.Inflation in the United States remains stuck near the 3.0% threshold. That persistent US inflation prevents the Federal Reserve from making the deep interest rate cuts that markets previously expected. Consequently, US Treasury yields remain elevated. High US yields typically pull investment capital away from emerging markets and keep the US dollar structurally strong.In Europe and China, the economic picture looks equally constrained. Eurozone growth sits near 1.0% while inflation hovers at 2.0%. China's economic expansion is projected to drop from 5.0% in 2025 to 4.0% by 2027. Under normal historical circumstances, a strong US dollar combined with weak Chinese economic demand would devastate Latin American currencies. However, the physical copper demand required for Artificial Intelligence infrastructure currently shields the Chilean Peso (CLP) and Peruvian Sol (PEN) from that traditional market damage.

2. Middle East Escalation and the Copper ParadigmSevere geopolitical shocks in the Middle East are fundamentally altering the global copper market. In early 2026, regional conflicts effectively closed the Strait of Hormuz. That specific maritime blockade trapped approximately 10 million barrels of crude oil per day, forcing production shutdowns and creating a massive global energy shock.An oil price spike usually hurts energy-importing nations by causing rapid currency depreciation. However, the 2026 Middle East conflict triggers a secondary, highly critical shock. The Middle East exports massive amounts of sulphur. Copper mining companies require sulphur as an indispensable chemical reagent to process, leach, and smelt copper ore.With sulphur exports blocked behind the Strait of Hormuz, global copper smelters face immediate operational paralysis. That specific supply chain fracture pushed benchmark copper futures past $5.98 per pound in early 2026. That elevated price represents a massive 39% year-over-year increase compared to January 2025.Because AI data centers require millions of miles of specialized copper cabling and heavy transformers, technology companies must buy copper regardless of the price. Therefore, copper now acts as a strategic safe-haven asset. The Chilean Peso and Peruvian Sol capture these safe-haven capital flows, partially disconnecting those Andean currencies from the standard risk-off sentiment that usually punishes emerging markets during geopolitical wars.

3. Supply-Side Bottlenecks in the AndesNevertheless, while global copper prices surge, Chile and Peru face severe internal operational barriers. Those domestic constraints prevent mining companies from simply pumping more copper into the market to capture high prices. The inability of the supply side to respond to price signals defines the current supercycle.Peru: Natural Gas Infrastructure Fracture

Peru currently faces a severe domestic energy crisis. In early 2026, the main natural gas pipeline operated by “Transportadora de Gas del Perú” ruptured. Peru relies heavily on natural gas, which accounts for roughly 60% of total national electricity capacity. Following the rupture, gas deliveries plummeted to just 10% of normal capacity.That pipeline failure directly threatens Peruvian copper production. The mining sector consumes 25% to 30% of Peru's national electricity demand. Copper processing requires uninterrupted baseload power. If the government forces industrial power cuts to save the residential grid, Peruvian copper output could drop significantly.Chile: Water Scarcity and Geological Degradation

Chile faces permanent, irreversible geological limitations. Mining companies are battling declining ore grades and severe water scarcity. To extract the exact same amount of copper today, companies must mine vastly more rock. That extraction process requires much higher capital expenditure and energy use, which compresses corporate profit margins.Production numbers clearly reflect those physical limits. Antofagasta (important mining area) Minerals reported a 1.6% drop in 2025 copper production due to water shortages. The Chilean state copper commission, “Cochilco”, recently downgraded its peak production estimates. “Cochilco” now projects that Chile's share of global copper production will fall from 23% in 2020 to just 21.5% by 2030.

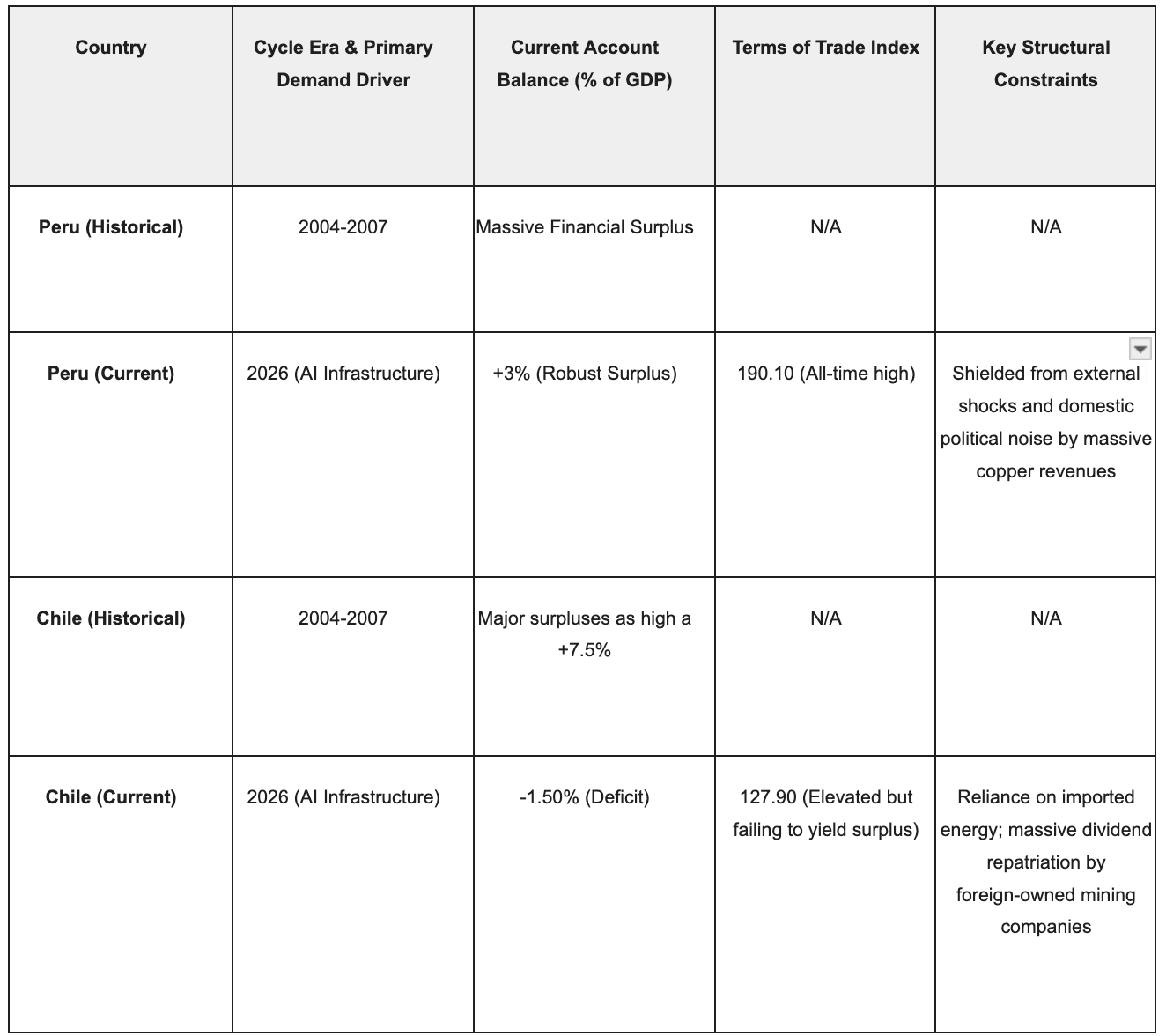

4. 2004–2007 Supercycle vs. 2026 AI DeficitComparing the 2026 AI environment to the 2004–2007 commodity supercycle reveals a major macroeconomic divergence between Chile and Peru. During the 2004–2007 cycle, rapid Chinese urbanization drove global copper demand. Both Andean nations generated massive financial surpluses during that era.In 2026, AI infrastructure drives the copper demand. Peru is successfully replicating its historical outperformance. Boosted by an all-time high Terms of Trade index of 190.10 points, Peru currently boasts a massive 3.0% Current Account surplus. That robust surplus protects the Peruvian Sol from external shocks and domestic political noise.Conversely, Chile completely fails to replicate its historical success. During the mid-2000s, Chile ran massive current account surpluses as high as 7.5% of GDP. Today, despite high copper prices and a Terms of Trade index of 127.90, Chile runs a Current Account deficit of -1.50% of GDP.That specific deficit occurs because Chile relies heavily on imported energy. The spike in global oil prices drastically inflates Chile's import bills. Furthermore, foreign companies own much of Chile's mining sector. Those foreign companies send their copper profits back to overseas parent companies as dividends. That profit repatriation drains money directly out of the Chilean economy, capping the upside potential for the Chilean Peso.

Policy Backdrop

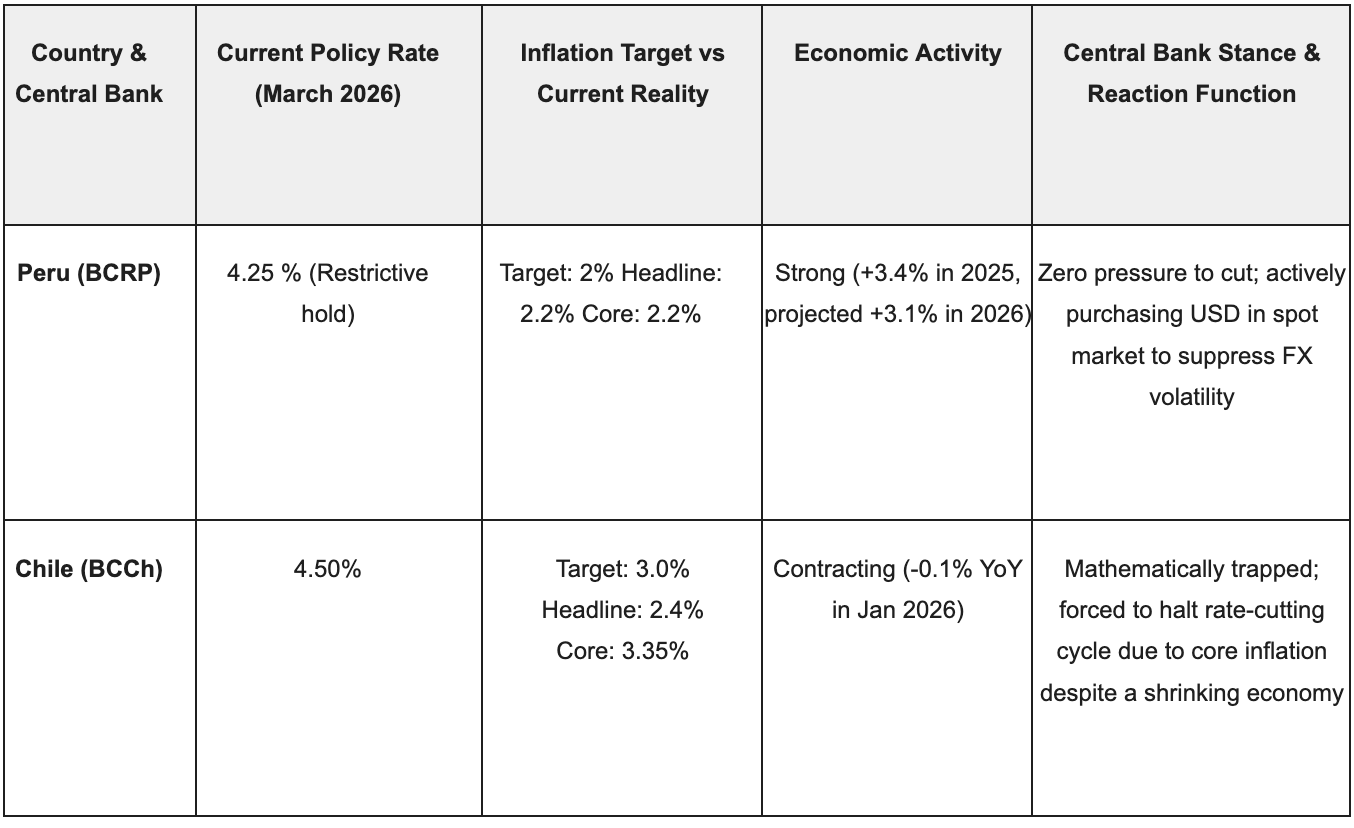

The physical copper demand from Artificial Intelligence provides a massive structural advantage for Chile and Peru. However, local political and monetary policies filter that structural advantage. The governments in Lima and Santiago must balance massive commodity revenues against sticky global inflation and acute domestic political transitions.1. Monetary Policy & Reaction FunctionsThe Central Reserve Bank of Peru (BCRP) and the Central Bank of Chile (BCCh) no longer mirror the United States Federal Reserve. Both Andean central banks operate on highly independent paths dictated by local inflation and economic output. Those specific policy choices directly impact the attractiveness of the Peruvian Sol (PEN) and Chilean Peso (CLP) for foreign exchange carry trades.The Central Reserve Bank of Peru (BCRP)

The BCRP operates under a highly orthodox, strict inflation-targeting framework. As of March 2026, the BCRP holds its benchmark policy rate at a slightly restrictive 4.25%. That specific rate decision marks the fifth consecutive meeting without a change.The BCRP targets a strict inflation band of 1.0% to 3.0%, with an explicit midpoint target of 2.0%. In February 2026, Peruvian headline inflation printed at exactly 2.2% year-over-year. Core inflation mirrored that headline number, also settling at 2.2%. Because 12-month forward inflation expectations sit tightly anchored at 2.1%, the BCRP maintains a restrictive real interest rate of approximately 2.15% to 2.31%.The central bank faces zero pressure to cut rates to stimulate the economy. Peruvian GDP expanded by 3.4% in 2025 and is projected to grow 3.1% in 2026. The BCRP is content to hold rates steady. Furthermore, the BCRP actively purchases US Dollars in the spot foreign exchange market. That direct intervention prevents the Peruvian Sol from becoming too volatile, ensuring the currency cleanly tracks the global copper price rather than domestic political noise.The Central Bank of Chile (BCCh)

The BCCh faces a much more complex and dangerous economic environment. In January 2026, the BCCh set its policy rate at 4.50%. Unlike Peru, Chile targets a strict 3.0% point target for inflation.On the surface, Chilean inflation looks controlled. February 2026 headline inflation printed at 2.4% year-over-year. However, the core inflation metric tells a highly problematic story. Core consumer prices rose 0.2% month-over-month to reach an annual rate of 3.35%. Because Chile imports almost all of its oil, the current Middle East energy shock directly inflates domestic transport and utility costs. Those elevated energy costs pass directly into core consumer prices.While copper supports the Chilean Peso, the domestic Chilean economy is contracting. January 2026 GDP shrank by 0.1% year-over-year. The BCCh is mathematically trapped. The central bank cannot aggressively cut interest rates to fix the contracting economy without causing an explosion in core inflation. Financial markets expect the BCCh to halt its rate-cutting cycle and hold a terminal rate of 4.00% to 4.25% by the end of Q1 2026.

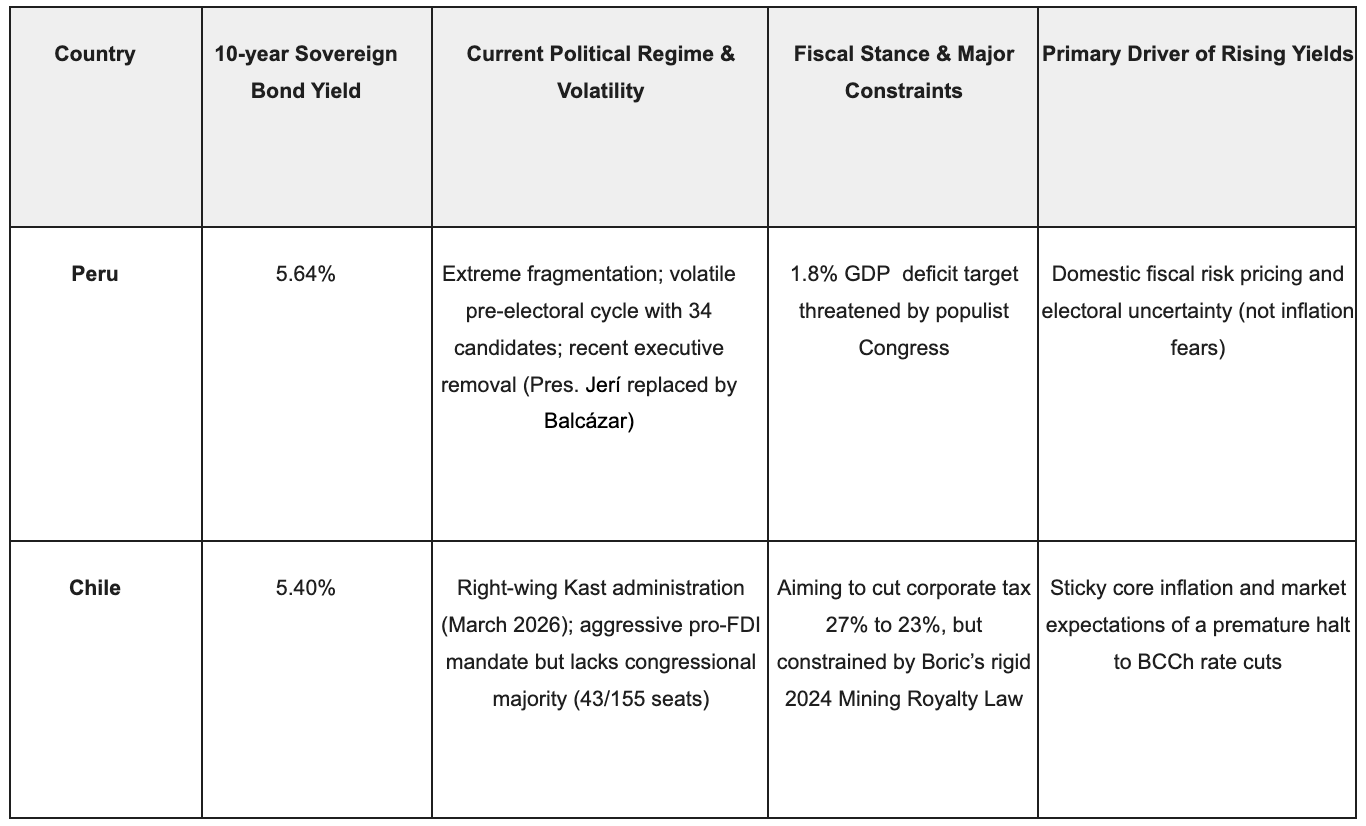

2. Peru: Institutional Friction and the 2026 ElectionsPeru exhibits remarkable macroeconomic stability despite chronic, deeply entrenched political dysfunction. The nation currently faces a highly volatile pre-electoral cycle. The general elections scheduled for April 12, 2026, will determine the presidency and the makeup of the newly reinstated bicameral Congress. That new Congress features a 60-seat Senate and a 130-seat Chamber of Deputies.Extreme fragmentation defines the Peruvian political landscape. A record 34 registered candidates are competing in the presidential race. That massive candidate pool heavily dilutes the vote. Early polling shows right-wing Lima mayor Rafael López Aliaga holding a slight lead of 12% to 15%. Keiko Fujimori trails at 7% to 9%. Neither candidate commands a decisive majority.Political instability peaked violently in February 2026. The Peruvian Congress executed a majority censure vote to remove President José Jerí over misconduct allegations. Congress hastily installed José María Balcázar as the new President just two months before the election.That continuous clash between the executive branch and the legislature threatens national fiscal targets. The Ministry of Finance legally targets a fiscal deficit reduction to 1.8% of GDP by 2026. However, a fractured Congress in an election year naturally leans toward populist spending. Congress recently authorized sweeping private pension fund withdrawals. That specific authorization engineers an artificial, debt-fueled consumption boom to appease voters.Despite the political chaos in Lima, the BCRP’s monetary credibility remains flawless. A structural firewall strictly separates the central bank from the legislature. The foreign exchange market recognizes that Peru possesses an independent central bank, exceptionally low public debt, and a massive 3.0% current account surplus. Those strong fundamentals allow the Peruvian Sol to completely ignore the political circus.3. Chile: The Kast Administration's Pro-Investment MandateChile is currently undergoing a violent political pendulum swing. Following the 2025 presidential election, right-wing President José Antonio Kast officially assumed office on March 11, 2026. That inauguration marks a total rejection of the state-centric, heavily regulated economic model favored by outgoing President Gabriel Boric.The Kast administration holds an aggressive mandate to resurrect Foreign Direct Investment (FDI). Kast explicitly aims to streamline mining permits and unlock Chile’s stalled copper extraction potential. His fiscal stance is aggressively pro-business. Kast formally proposes slashing the corporate income tax rate from 27% to 23%. He also proposes eliminating capital gains taxes on low-value equity trades to deepen domestic capital markets. In a highly symbolic move, Kast immediately merged the Ministries of Mining and Economy under the leadership of Daniel Mas. That merger signals the government will treat mining as an economic engine rather than an environmental liability.However, legislative mathematics severely limit Kast’s power. The President lacks an absolute majority in the bicameral Congress. Kast controls only 43 seats in the 155-seat Chamber of Deputies. To pass legislation, his coalition must negotiate transactionally with swing blocs. Kast relies heavily on Franco Parisi's populist Partido de la Gente, which controls 14 crucial seats.Furthermore, Kast inherits a heavy, rigid fiscal architecture from the previous administration. President Boric implemented the 2024 Mining Royalty Law. That law imposes a 1% flat tax on total copper sales and a highly progressive secondary tax on operating income. The law caps the maximum effective tax burden at 46.5% of pre-tax earnings for large operators.That 46.5% tax ceiling severely damages corporate profit margins. It alters the Net Present Value calculations for global mining conglomerates, forcing foreign companies to demand higher financial returns before committing capital to Chile. The core question for the Chilean Peso is whether Kast’s tax cuts and streamlined permits can offset the heavy burden of the Boric royalty law.4. Yield Curve and Forward Guidance DivergenceThe structural transition of the macro environment shows up clearly in the fixed income markets. Sovereign yield curves currently expose a growing disconnect between what central banks want and what the market expects. Global macroeconomic constraints are actively overriding local monetary intentions.In Chile, the BCCh wants a gradual reduction of the policy rate to support weak domestic growth. However, the Chilean sovereign curve prices in a much slower easing path. As of March 2026, the yield on the Chilean 10-Year Government Bond stands at 5.40%. The bond market effectively rejects the BCCh’s disinflationary optimism. Driven by the Middle East energy shock and sticky 3.35% core inflation, traders expect the BCCh to halt rate cuts prematurely.In Peru, a similar dynamic pushes yields higher for entirely different reasons. The BCRP successfully controls inflation at 2.2%. However, the yield on the Peruvian 10-Year Government Bond recently climbed to 5.64%. That upward pressure reflects domestic fiscal risk pricing, not inflation fears. Bond investors demand a higher premium to hold long-term Peruvian debt through the volatile April 2026 election cycle and the populist pension withdrawals.Ultimately, both the BCCh and BCRP maintain structurally high real interest rates compared to advanced economies. Those high rates provide robust carry trade metrics for the Chilean Peso and Peruvian Sol. Combined with massive dollar inflows from the AI copper supercycle, those fixed-income metrics erect an impenetrable macroeconomic fortress around the Andean currencies.

Current Market Synthesis and Institutional Positioning

An absolute physical constraint defines the global macroeconomic architecture in March 2026. The artificial intelligence build-out collides directly with finite copper supplies. That physical bottleneck dictates pricing in the sovereign debt and foreign exchange markets of the Andean region.

The foreign exchange options market actively quantifies that structural shift. Options traders use a metric called “risk reversals” to measure the price difference between call options and put options. A high premium normally indicates that investors fear a sudden currency crash. Today, the 1-month and 3-month risk reversals for the USD/CLP and USD/PEN pairs show a total collapse in that premium. Institutional capital no longer pays up to protect against sudden depreciations in the Chilean Peso or Peruvian Sol.Implied volatility for the USD/CLP 1-Month contract currently sits severely compressed between 3.39% and 4.02%. That tight range places Chilean Peso volatility near its absolute post-pandemic bottom. Options market makers view a violent, unhedged crash in the Andean currencies as highly improbable. The sheer volume of incoming copper revenues provides a massive valuation buffer.Institutional flow data confirms that pricing reality. Macro hedge funds and real-money accounts are executing a synchronized accumulation of Andean assets. Top-tier trading desks actively recommend shorting the Canadian Dollar against the Chilean Peso (Short CAD/CLP). That specific trade captures the outperformance of copper over broader global trade proxies while earning a 200 basis point interest rate advantage.Foreign Direct Investment (FDI) permanently anchors those capital flows. Amazon recently announced a $4 billion direct investment to build data centers in Chile. Peru boasts a $15.8 billion public-private infrastructure pipeline. In early March 2026, the Peruvian environmental agency SENACE approved the $3.4 billion Trapiche copper project. That single regulatory approval forces global corporations to systematically buy Peruvian Soles to fund localized, multi-year construction costs.Trend AnalysisTrend Analysis

The most immediate confirmation of the Andean thesis exists in the microstructure of the London Metal Exchange (LME). The LME copper futures curve currently operates in severe backwardation. Backwardation occurs when the spot cash price trades higher than future delivery months. That pricing structure signals acute physical scarcity. Industrial consumers willingly pay heavy premiums to secure physical copper immediately rather than wait for future production.Copper inventories dropped so fast in early 2026 that the LME instituted emergency regulatory rules. The exchange capped the daily cost of rolling short-term contracts at 0.50% and forced large position holders to lend metal at a 0.25% daily rate. When a primary global exchange alters its fundamental rules to prevent a physical short squeeze, the action definitively proves that demand structurally overwhelms supply.United States technology companies drive that overwhelming demand. Top hyperscalers (Microsoft, Alphabet, Amazon, Meta, and Oracle) project a staggering $700 billion in aggregate capital expenditure for 2026. Data centers require massive electrical transformers and heavy copper wiring for power distribution and liquid cooling. That $700 billion infrastructure sprint acts as an impenetrable price floor for global copper.However, strict institutional risk management requires analyzing contrasting data. Two real-time headwinds threaten the Andean FX appreciation thesis:Absolute US Dollar Strength: In February 2026, the US labor market unexpectedly lost 92,000 jobs, pushing unemployment to 4.4%. That localized economic fear triggered a massive global risk-off reflex. Capital fled into the safety of the US Dollar, pushing the Dollar Index (DXY) to 99.38. Absolute US Dollar strength exerts mechanical, downward pressure on all emerging market currencies, regardless of copper prices.Technological Substitution: Heat generation remains the ultimate constraint inside AI data centers. Semiconductor firms are aggressively developing optical interconnects. Optical systems move data using light rather than electrical signals over copper wires. If technology companies successfully replace copper wiring with optical interconnects at scale, a massive vector of future copper demand disappears.

2. The Indicator Framework: Leading vs. Lagging SignalsInstitutional capital allocation requires a strictly forward-looking data framework. Traditional macroeconomic models rely heavily on lagging indicators. Those lagging metrics are currently useless for trading the USD/CLP and USD/PEN exchange rates.Trailing Gross Domestic Product (GDP), ex-post current account balances, and headline Consumer Price Index (CPI) prints reflect a macroeconomic reality that derivatives markets already priced in months ago. For instance, the Chilean economy expanded by a marginal 0.6% in the fourth quarter of 2025. Utilizing that backward-looking growth print to short the Chilean Peso completely misses the explosive, real-time demand occurring in global physical metal markets.The forward-looking institutional thesis relies exclusively on high-frequency, leading indicators:Smelter Treatment Charges: These charges reflect raw copper availability relative to global smelting capacity. Declining treatment charges signal tightening raw material conditions weeks before physical shortages impact the spot cash price.Hyperscaler Corporate Debt: Technology companies issued over $200 billion in investment-grade bonds in 2025 to fund the AI build-out. Tracking that debt syndication provides an exact leading signal of future industrial metal demand. Borrowed capital immediately converts into physical infrastructure procurement.Sovereign 5-Year Bond Yields: Sovereign yields strip away retail noise to measure pure institutional capital flows. In early March 2026, the Chilean 5-Year Government Bond yield compressed rapidly from 5.170% down to 4.945%. The Peruvian 5-Year yield dropped to 4.416%. Plunging yields signal that foreign institutions are aggressively buying Andean government debt. To buy that debt, those institutions must cross the bid-ask spread and purchase local Chilean and Peruvian currency first.

3. Regional Divergences: The USD/CLP and USD/PEN DynamicsThe historical financial relationship between the United States and the Andean bloc is completely broken. Over the past 20 years, the US Dollar Index (DXY) and global copper prices maintained a strict inverse correlation. When the US Dollar strengthened, copper prices fell. In March 2026, the DXY trades near the 100.00 threshold, yet copper prices continue surging. The sheer physical necessity of AI infrastructure overrides the traditional financial gravity of a strong US Dollar.Real yield differentials heavily fortify the Chilean Peso and Peruvian Sol. Nominal yields only tell half the story. Institutional investors track the real yield, calculated by subtracting expected inflation from the nominal bond yield.Currently, the US 10-Year Treasury yields 4.30%. The Chilean 10-Year sovereign bond yields 5.52%. The Peruvian 10-Year bond yields 5.90%. Because the central banks in Chile and Peru controlled inflation aggressively, their real yields remain deeply positive. Global fixed-income managers get paid excellent real returns to hold Andean debt. That positive yield differential neutralizes the capital flight that usually devastates emerging markets when the US Dollar surges.While both currencies benefit from copper, their volatility profiles differ drastically. The Chilean Peso operates as a free-floating currency. The Central Bank of Chile allows the exchange rate to absorb macroeconomic shocks. The USD/CLP pair exhibits high volatility, making the currency a preferred vehicle for macro hedge funds looking for large, directional trades.Conversely, the Peruvian Sol operates under a "dirty float" mechanism. The Central Reserve Bank of Peru actively intervenes in the foreign exchange market, using its massive dollar reserves to suppress both upward and downward price spikes. That intervention transforms the USD/PEN pair into a structurally low-volatility asset. Institutional investors treat the Peruvian Sol as a stable, fixed-income substitute rather than a volatile trading instrument.4. Technical ArchitectureThe technical architecture confirms a sustained structural uptrend. The 50-day Simple Moving Average (orange) maintains a dominant "Golden Cross" above the 200-day Simple Moving Average (blue). Immediate institutional downside risk is strictly contained by the horizontal support channels defined at the $5.63 and $5.54 levels.

The pair exhibits a severe macroeconomic breakdown. After establishing an institutional floor near 850.00, the resulting relief rally met absolute technical rejection. The blue arrow highlights the exact point of confluence where the 200-day Simple Moving Average (930.87) and the Fibonacci resistance ceiling (931.97) mathematically cap US Dollar strength.

Bollinger Band mapping visualizes aggressive central bank market intervention. The extreme mathematical compression (the "squeeze") from November through February proves the BCRP's successful suppression of volatility. The violent March 2026 US Dollar breakout was immediately neutralized at the upper band (3.5072), confirming the fundamental downward trajectory of the pair.

Forward-Looking Scenario Analysis

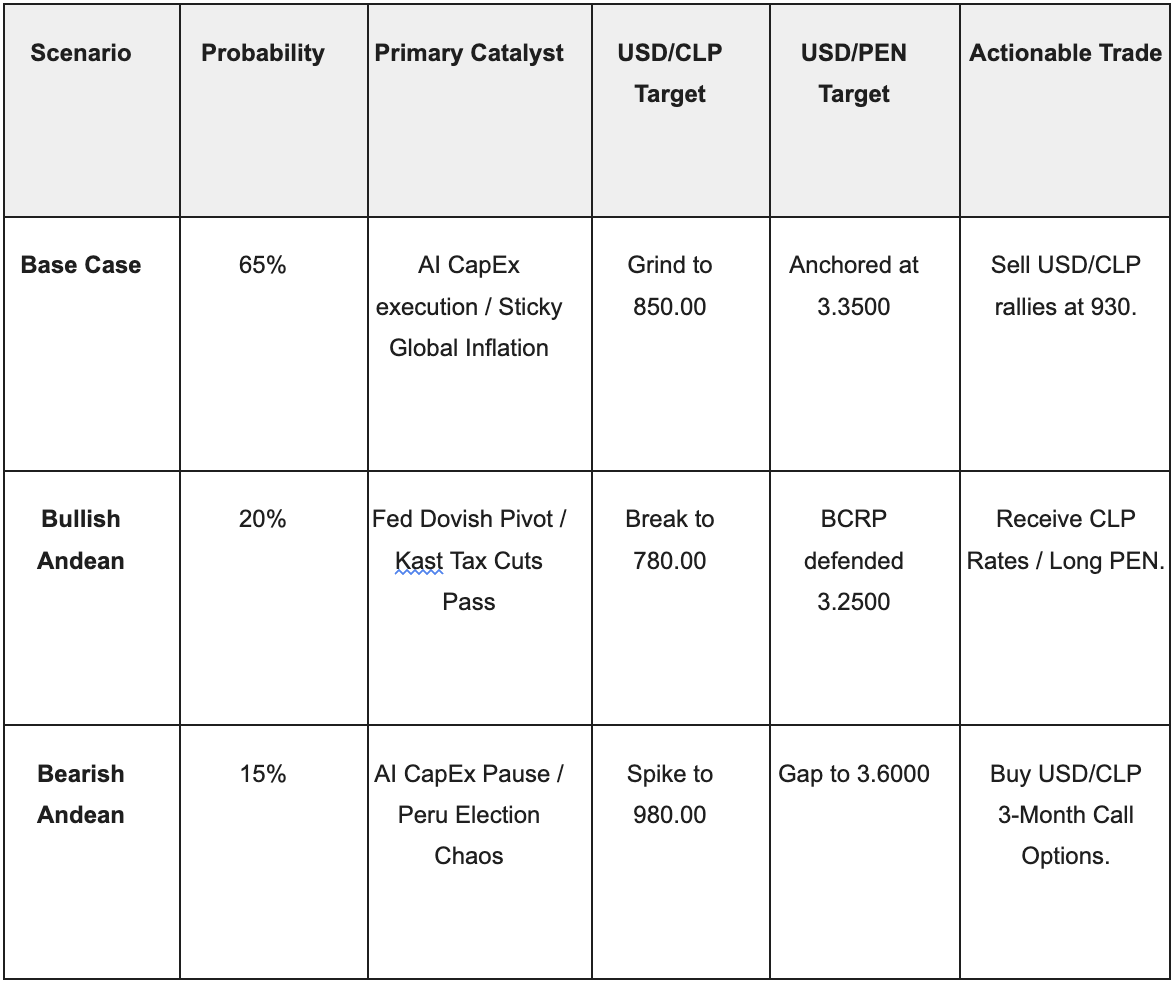

The macroeconomic architecture of the Andean region is shifting rapidly. The historical correlation matrix binding the Chilean Peso (CLP) and Peruvian Sol (PEN) to broad emerging markets is broken. This structural decoupling is permanent. It is the direct consequence of the AI infrastructure supercycle hitting physical copper limits.The global economy now demands vast physical energy and materials. Mean-reverting assumptions are obsolete. Andean currency valuations are now tied to hyperscale data center deployments and sovereign policy reactions.Currently, the options market is mispricing this regime. Volatility is compressed. Markets are ignoring fat-tail risks. These risks include semiconductor supply chain failures, central bank divergences, and Peruvian electoral chaos.We define three rigid, probability-weighted paths for the April to September 2026 horizon. These are engineered market trajectories, not speculative forecasts. They map the transmission between global supply chains, local policy, and institutional order flow.1. Base Case (Probability: 65%) - The Structural GrindThe Base Case envisions a sustained equilibrium. Physical AI infrastructure demands dictate a permanent upward re-rating of Andean terms of trade. This path requires no speculative blow-off top. It relies on baseline hyperscaler deployment and rigid central bank policy. The market experiences a systematic grind. Realized volatility remains low.The Copper Floor and Sticky US Inflation

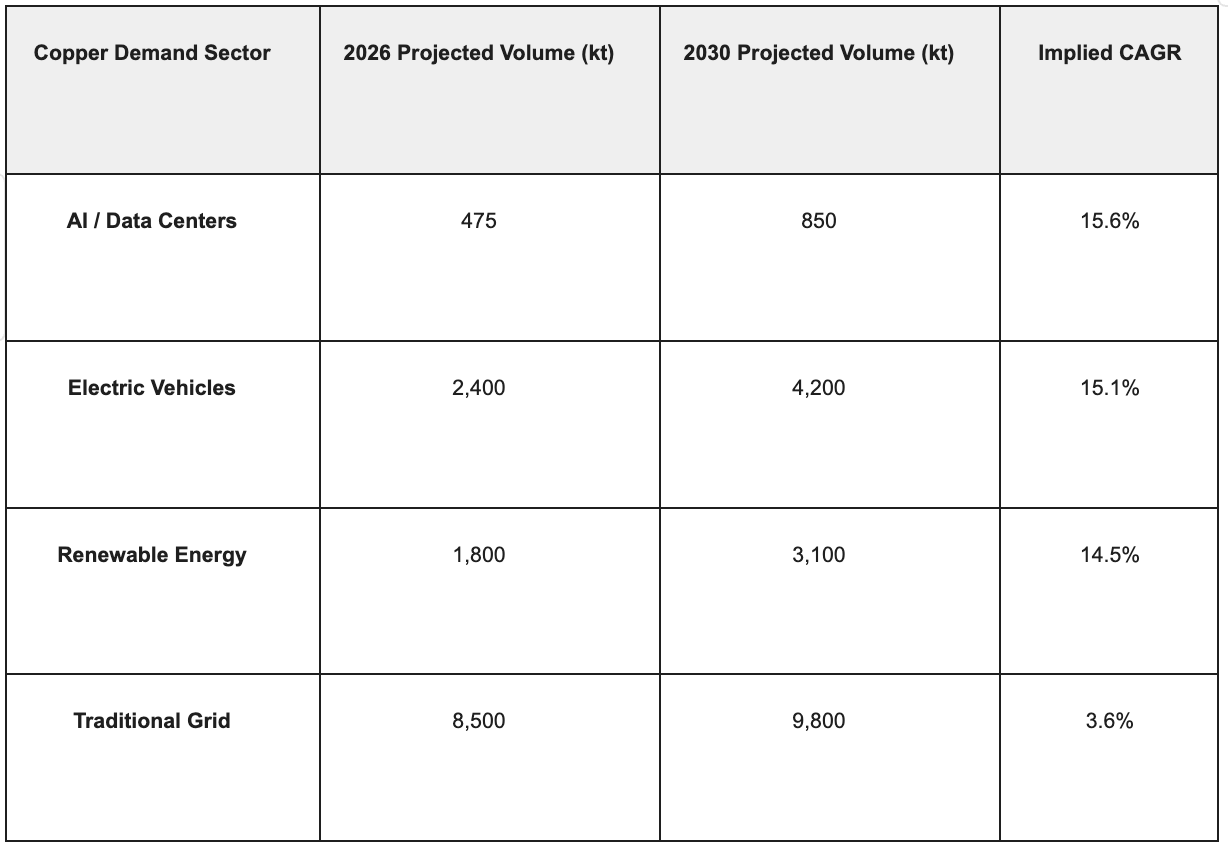

Copper spot prices remain elevated. They consolidate in a tight $5.30 to $5.70 range. Physical capital expenditure from tech conglomerates maintains this floor. The market narrative shifts from software capabilities to physical power distribution.Data center copper demand tracks toward 572,000 tonnes annualized. This functions independently of business cycles. Baseline AI copper demand will grow at a 15.6% compound annual growth rate (CAGR) through 2030.

The US economy avoids a cyclical recession. However, domestic US price pressures remain sticky. The Federal Reserve cannot execute a sustained easing cycle. This "higher-for-longer" yield environment caps emerging market risk assets. It prevents copper from breaking above $6.00.

Divergent but Rigid Central Banks

Andean central banks prioritize inflation expectations over aggregate demand.In Peru, the BCRP holds its rate at 4.25%. Headline and core inflation recently rebounded to 2.2%. Supply-side shocks drive this pressure. The BCRP prioritizes stability in a partially dollarized system. Rate cuts are off the table. The 4.25% floor compresses the yield differential against the US dollar.In Chile, the BCCh maintains a hawkish pause at 4.50%. Chile battles energy-driven core inflation. Diesel tax changes have increased industrial operational costs. The BCCh prioritizes its 3% target. This restrictive floor supports the CLP but stifles domestic credit.Systematic Order Flow

The BCRP systematically intervenes in the spot market. The USD/PEN compresses near 3.3500. The central bank acts as a market maker to absorb mining inflows. This suppresses volatility and frustrates momentum traders.The USD/CLP grinds slowly downward toward 850.00. Mining treasurers systematically sell USD forward to fund domestic operations. This creates a massive rolling ceiling. The BCCh's 4.50% rate deters carry trades. Algorithmic models add to short USD positioning.2. Upside Scenario (Probability: 20%) - The “Copper Squeeze & Policy Pivot”This path is a violent, positive convexity event. It requires US monetary capitulation and aggressive Chilean fiscal policy.Fed Capitulation and Kast Fiscal Shock

The US labor market fractures. The Federal Reserve executes an emergency dovish pivot. The US Dollar Index (DXY) collapses. Institutional capital rotates into commodities. Copper violently breaks the $6.00 threshold.Simultaneously, Chilean President Kast passes radical tax reform. Corporate income taxes drop to 23%. Capital gains taxes on small equity trades are eliminated. This rewrites the net present value for global miners. A massive wave of front-loaded Foreign Direct Investment (FDI) floods Chile.Violent Breakouts

The USD/CLP shatters the 850.00 floor. Corporate hedgers are caught offside. A massive gamma squeeze accelerates the collapse. The pair targets 780.00. The BCCh allows unchecked appreciation to import deflation and achieve its 3% target.In Peru, the BCRP faces asymmetric pressure. Uncontrolled PEN appreciation threatens export competitiveness. The BCRP executes massive spot purchases. It artificially caps the Sol at 3.2500. The central bank heavily sterilizes these purchases to protect local interbank rates.3. Downside Risk Scenario (Probability: 15%) - “CapEx Pause & Electoral Contagion”This is a severe tail-risk event. It features a systemic failure of the AI supply chain and Andean political stability.Optical Interconnect Failures

Hyperscale data centers hit an interconnect bottleneck. Legacy copper cabling fails at extreme power densities. The industry must transition to advanced optical inputs. However, manufacturing bottlenecks stall this transition. Tech behemoths pause Q3 and Q4 2026 construction guidance.Anticipated copper demand vanishes. Speculators liquidate. Copper spot prices gap down below $5.00. The structural terms-of-trade advantage evaporates.Electoral Contagion

Peru's April 2026 elections descend into fragmentation. Extreme populist candidates surge in the polls. They promise to nationalize the Camisea gas pipeline. This threatens free-trade pacts and foreign investment. Capital flees Peruvian assets.Carry Trade Unwind

Institutional carry trades unwind violently. The USD/CLP gaps higher. It slices through the 200-day moving average at 930.00. Automated stop-loss buying accelerates the collapse. The pair targets 980.00.In Lima, the capital flight ruptures the USD/PEN Bollinger Band ceiling. The BCRP abandons tactical smoothing. It burns FX reserves rapidly to defend the 3.6000 level. The controlled-float regime fails systemically.4. 6-Month Forward Scenario Probability Matrix (USD/CLP & USD/PEN)

Key Catalysts, Timeline, and Risks to the Thesis

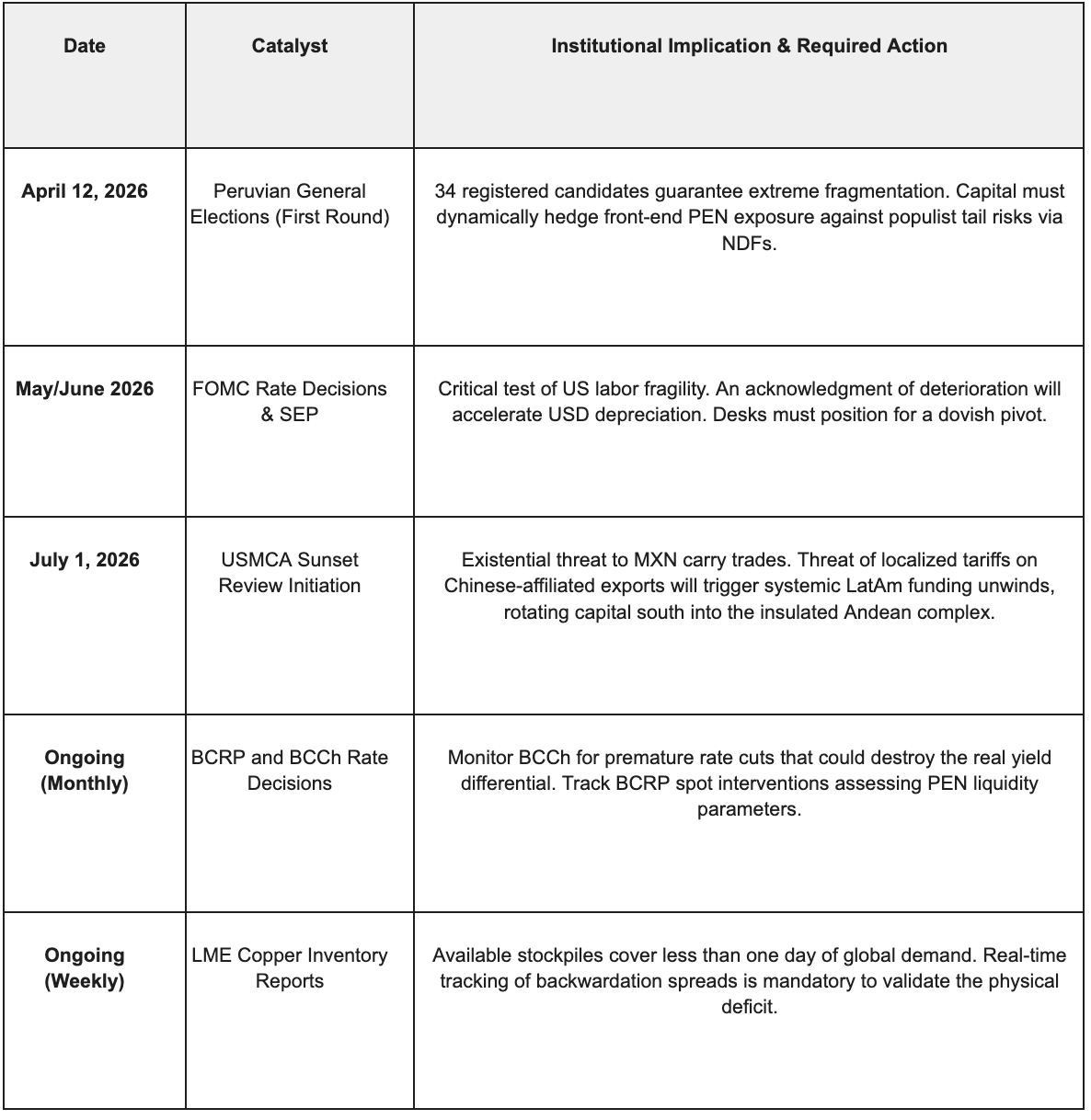

The structural decoupling of the Chilean Peso (CLP) and Peruvian Sol (PEN) relies on the unyielding physical constraints of the AI infrastructure build-out. However, institutional portfolios must navigate a dense concentration of political, monetary, and trade-related events over the next two quarters. Successful execution requires rigid adherence to the upcoming catalyst calendar and continuous recalibration of the risk matrix.1. 6-Month Catalyst Calendar (April – September 2026)

2.Risk Matrix

Elite institutional risk frameworks must isolate and hedge against three specific vectors capable of invalidating the thesis:Data Risks: A sudden exogenous energy shock forcing US inflation back above 4% would trigger Fed hikes, flattening the SOFR curve and draining EM capital. Alternatively, a non-linear collapse in Chinese property and shadow-banking sectors could wipe out baseline copper demand, entirely masking the incremental AI infrastructure deficit and driving spot prices below $5.00/lb.

Policy Reaction Risks: The BCRP prematurely abandoning its aggressive "dirty float" intervention would strip the PEN of its artificial volatility dampener, destroying its utility as a stable cash-equivalent. In Chile, the BCCh capitulating to political pressure and cutting rates too aggressively would collapse the real yield differential against US Treasuries, triggering systemic capital flight regardless of copper prices.

Market Microstructure Risks: The LME escalating administrative interventions to artificially halt copper backwardation would sever the organic price discovery mechanism, preventing the CLP from capturing the true physical clearing price of the metal. Additionally, sudden illiquidity or widening bid-ask spreads in Andean non-deliverable forward (NDF) markets would create toxic execution slippage, trapping institutional capital.

Conclusion

1. The Structural RealityThe artificial intelligence infrastructure build-out has permanently altered the supply-demand physics of global copper, fundamentally transforming the Chilean Peso and Peruvian Sol from high-beta, cyclically vulnerable EM proxies into structurally supported, low-volatility fortress assets. The exponential, non-negotiable energy density requirements of localized AI data centers, colliding with structurally stagnant global mine supply and depleted exchange inventories, have detached copper pricing from traditional Chinese property cycles. For Andean sovereign balance sheets intrinsically anchored by export revenues, this physical scarcity translates directly into unprecedented terms-of-trade invulnerability, decoupling the CLP and PEN from broader emerging market volatility to establish a new paradigm of intrinsic capital accumulation.2. Dominant Market BehaviorInstitutions must abandon legacy Latin American allocation models and adopt a highly specific, asymmetric execution manual. First, initiate systematic accumulation of Andean local currency sovereign debt, prioritizing the 5-to-7-year duration segment to capture the optimal blend of term premium and real yield protection. Second, foreign exchange desks must aggressively sell USD rallies against the CLP, utilizing automated execution algorithms to short USD/CLP at standard deviation bands above the 50-day moving average. Finally, corporate treasuries must repurpose their utilization of the Peruvian Sol; backed by the BCRP's ruthless volatility suppression, the PEN functions as an ultra-stable cash-equivalent for parking LatAm-allocated liquidity via overnight repo agreements.3. Patience vs. ReactivityNavigating this paradigm requires a ruthless delineation between macroeconomic variables demanding multi-quarter patience and acute catalysts requiring millisecond reactivity. Extreme patience is required regarding the macro-level translation of physical AI CapEx—securing real estate, building facilities, and laying high-voltage cabling—into official sovereign current account surplus data. Conversely, extreme reactivity is mandatory for binary tail risks. An unexpected surge by an anti-mining populist in the Peruvian elections, or a sudden, statistically confirmed collapse in US Non-Farm Payrolls, demands instantaneous dynamic hedging and rapid exposure recalibration before central banks or broad market consensus can react.4. Final ThoughtOver the next macroeconomic cycle, financial markets will disproportionately and systematically reward those who deeply understand inelastic physical supply chain constraints and localized central bank policy reaction functions—not just those trading headline US macroeconomic data.