The Failed Acquisition of Banco Sabadell by BBVA

Deal Overview

Hostile public takeover bid (all-share tender offer) by BBVA for Banco Sabadell structured under Spanish takeover law and supervised by the National Securities Market Commission (CNMV) and National Markets and Competition Commission (CNMC).

● Parties: Banco Bilbao Vizcaya Argentaria, S.A. (BBVA, bidder); Banco de Sabadell, S.A. (Sabadell, Target).

● Total Transaction Size: Initial offer of €14.8 billion later increased by 10% to approx. €17 billion following regulatory clearance and market pushback.

●Transaction structure: Consideration to be delivered through a share-for-share exchange, evolving from one BBVA share (plus a small cash component) for every 〜5.5 Sabadell shares, to later a pure all-share offer of one BBVA share for every 〜4.8 Sabadell shares.

● Public announcement date: BBVA first announced the bid in May 2024 after its friendly approach was rejected.

● Status: Having previously been denied by regulators, the offer was formally launched again following CNMV authorisation in September 2025, with the revised €17 billion terms; the bid ultimately failed to secure the required level of shareholder acceptances.

BBVA’s eventually hostile takeover bid for Banco Sabadell, a contested all-share transaction valued at up to €19 billion, emerged in 2024 against the backdrop of political scrutiny of such deals in Spain. The proposal aimed to combine Spain’s second- and fourth-largest listed banks, using a share-exchange structure. Strategically, BBVA sought scale, cost synergies and a stronger domestic presence.Sabadell’s board defended a stand-alone growth plan and argued that the offer fundamentally undervalued its prospects. This clash played out in an environment shaped by intense regulatory and governmental oversight with Spanish authorities imposing conditions on any full integration.

Company Details

Acquirer - BBVA

● Founded: 1857 (Bilbao)

● CEO at time of bid: Onur Genc

● Market valuation at launch: €50-55 billion equity value around the initial 2024-2025 bid window.

● Sector: Diversified universal bank; retail, commercial, corporate and investment banking, asset management, and insurance, with a strong digital and emerging markets focus.

BBVA traces its origins to the Banco de Bilbao, founded in 1857, and took its current form in 1999 through the merger of Banco Bilbao Vizcaya with Argentaria, a state-owned banking conglomerate that had itself been created to consolidate Spain's public financial institutions in the early 1990s. That foundational merger was a direct product of the broader consolidation wave sweeping European banking as institutions repositioned ahead of monetary union, and it established the template for BBVA's subsequent strategy: growth through acquisition and geographic diversification rather than organic domestic expansion alone.

The external environment BBVA has had to navigate since that formation has been demanding. BBVA's growth strategy, especially in the wake of financial crisis leaned into its international diversification, with its Mexican franchise - built through the acquisition of Bancomer in 2000 - acting as a critical earnings buffer during the years when Spanish net interest margins were compressed to historic lows under the ECB's accommodative rate regime. Mexico today generates the majority of BBVA's group profit, which distinguishes it from a purely European banking story and gives it an exposure profile that is less correlated to the eurozone cycle than its balance sheet size might suggest.

Divestment of BBVA USA to PNC Financial Servicesfor approximately $11.6 billion (2021). The sale reflected a judgment that achieving meaningful scale in the fragmented and intensely competitive US retail market would require capital commitments disproportionate to the likely return. The exit crystallised a significant capital surplus that BBVA subsequently directed toward share buybacks and, ultimately, toward the capital position that underpinned its bid for Sabadell.

On the product and capability side. BBVA's core offering spans retail and private banking, SME and corporate lending, investment banking, asset management, and insurance. BBVA has consistently ranked among the leading banks globally for mobile banking functionality, and its data analytics and AI infrastructure underpin both customer acquisition and credit risk management across geographies with very different regulatory and macroeconomic profiles. This has driven strong customer growth and improved cost efficiency ratios relative to more traditionally structured European peers. Combined with high returns on equity, driven disproportionately by Mexico and Turkey's Garanti BBVA, and a distribution network spanning over 25 countries, BBVA enters the Sabadell transaction as a group with considerable financial power but also one with strategic imperatives around European scale that the domestic disposal of BBVA USA left unresolved.

Target - Sabadell

● Founded: 1881 (Catalonia)

● CEO at time of bid: Cesar Gonzalez Bueno.

● Market Valuation at launch: Roughly €12 billion equity value around the offer window.

● Sector: Commercial and retail banking group focused on SMEs, corporates and retail clients, also having UK presence as owner of TSB (at the time).

Banco Sabadell was founded in 1881 in Sabadell, an industrial town in Catalonia, by a group of businessmen and industrialists who required a local institution capable of financing commercial activity that the major Madrid-based banks were poorly positioned to serve. That founding purpose, providing sophisticated financial services to entrepreneurial, commercially active clients, has remained the organising principle of Sabadell's identity throughout its evolution, and it is the source of its enduring competitive differentiation in the SME and mid-market corporate segment.

The external environment Sabadell has had to navigate over the past fifteen years has been among the most severe in modern European banking history. Pressure came from the regulatory and structural response to the crisis: the forced recapitalisation of Spanish savings banks, the creation of Sareb (the state “bad bank”) and the broader rationalisation of Spanish banking that followed produced a period of accelerated consolidation in which mid-sized institutions faced a choice between acquiring distressed competitors to build scale or risking marginalisation behind dominant groups. Sabadell chose the acquisitive route, absorbing Banco Guipuzcoano in 2010, Banco CAM in 2012, and Banco Gallego in 2013; transactions that substantially enlarged its balance sheet and deposit base but also brought integration costs and inherited asset quality problems that weighed on the group for several years.

The most strategically ambitious and ultimately problematic of Sabadell's expansion decisions was the acquisition of TSB from Lloyds Banking Group in 2015: for approximately £1.7 billion. TSB offered a British retail franchise with a clean balance sheet, a known brand, and a regulatory environment that would allow Sabadell to build a meaningful international earnings stream outside the compressed Spanish market. In practice, it was damaging. The 2018 IT migration of TSB onto Sabadell's banking platform (intended to extract cost synergies) resulted in a systems failure that locked hundreds of thousands of customers out of their accounts for an extended period, triggered regulatory investigations, remediation costs, and reputational damage on TSB.. By 2024, Sabadell had agreed to sell TSB to Santander UK for approximately £2.65 billion.

The domestic refocusing that followed the TSB disposal has clarified what Sabadell genuinely does well. Its core strength remains the depth of its relationships with Spanish SMEs and mid-market corporates, a segment that requires tailored credit assessment, active relationship management, and product breadth across lending, cash management, trade finance and hedging instruments that purely digital challengers have not yet replicated at scale. Sabadell's structural position in Spanish banking remains challenged: it operates in a market dominated by CaixaBank and the domestic operations of Santander and BBVA, where the cost advantages and distribution reach of the larger groups exert persistent competitive pressure on mid-tier institutions. That context is what made Sabadell the target of BBVA's approach.

Mapping Out The Bid - The Acquisition

Timeline

Type of deal: Hostile public takeover bid (acquisition), structured as an all-share tender offer by BBVA for 100% of Banco Sabadell’s share capital under Spanish takeover rules.

Headline Purchase Price

Initial hostile offer, May 2024 - est. €13 billion

Subsequent adjustments, 2024 - offer tweaked (see below) to preserve value around €13.4 billion as dividends and share-price evolved.

Formal bid phase, Sept. 2025 - publicly framed around €14.8 billion at launch, then increased by 10% with BBVA later citing an equivalent value approaching €19 billion at peak share prices.

Implied Price per Share

Initial exchange ratio - 1 new BBVA share for every 4.83 Sabadell shares. Representing roughly a 30% premium to Sabadell’s closing price on 29 April 2024.

Interim structure - 1 BBVA share for 5.5483 Sabadell shares + cash component of around €0.13 per share (linked to dividend adjustments by Sabadell).

Final improved ration - 1 BBVA share for every 4.8376 Sabadell shares on an all-share basis, increasing by 10% relative to the initial CNMV filed bid.

April 2024, Friendly approach

BBVA sends a merger proposal to Sabadell’s board, which rejects it in early May 2024 as undervaluing the bank.

9 May 2024, Public hostile announcement

BBVA publicly announces an all-share hostile takeover bid for Sabadell, offering 1 BBVA share for every 4.83 Sabadell shares, giving an initial value of around €12.2 billion

Mid-late 2024, Adjustments and regulatory process

As both banks pay dividends and share prices move, BBVA adjusts the mid, including a small cash component, to keep the value broadly stable at around €13.4 billion

24 June 2025, Government merger authorisation (with conditions)

Spain’s council of Ministers authorises the ‘economic concentration’ of BBVA and Sabadell but imposes a three year obligation to maintain separate legal entities, equity and autonomous management.

5 September 2025, CNMV approval of takeover prospectus

CNMV authorises the takeover bid; BBVA sets the acceptance period to start on 8 September 2025

8 September 2025, Opening of acceptance period

Sabadell shareholders are formally able to tender their shares; the offer at this point is publicly described as a hostile bid valued at about €14.8 billion.

21-22 September 2025, Improved offer terms

BBVA increases the offer’s economic value by about 10%, taking the value to around €19 billion.

October 2025, Close of acceptance period

The one-month acceptance window ends.

15-17 October 2025, Bid lapse

The offer is accepted by only around 25% of Sabadell’s share capital and voting rights, below the 30% minimum acceptance condition, so the bid automatically lapses and does not complete.

Sabadell announces it will continue as an independent bank; BBVA simultaneously communicates an acceleration of shareholder-remuneration plans after the failed transaction.

Motivation

For BBVA, the bid was framed as a growth transaction designed to consolidate its position in Spain and create one of Europe’s most competitive and innovative banks. Management repeatedly highlighted three things: scale, synergies and strategic repositioning of its Spanish branch. It saw the combination as a way to deepen its home market presence in profitable retail and SME segments, close the gap with competitors such as Santander, and gain stronger pricing power in a market where three universal banks would dominate roughly two‑thirds of activity. BBVA targeted around €850-900 million of annual pre‑tax synergies by 2028, primarily from cost savings in overlapping branch networks, IT and operations, and from funding and capital efficiencies needed to support the digital transformation. The deal was also positioned as enabling an extra €5 billion of yearly lending to households and businesses and enhancing BBVA’s ability to compete on innovation, by using Sabadell’s regional strengths to scale its digital banking model.

Sabadell’s board did not regard the proposal as an attractive avenue for value creation; instead, its motivation in engaging with the process was defensive and oriented towards preserving its standalone strategy. The board’s formal report to the CNMV argues that the offer “destroys shareholder value,” undervaluing Sabadell’s strategic plan, and that the bank could deliver higher returns as an independent entity. Its management argued it had already embarked on a successful restructuring and growth trajectory, with improving profitability, better asset quality, and a clear focus on domestic SME and retail banking.

The board pointed to potential revenue losses and dis‑synergies from client attrition, cultural friction, and branch rationalisation, particularly in regions where both banks have strong, overlapping presence. By contrast, Sabadell’s own strategy, (including the agreed sale of TSB and an extraordinary dividend and buyback programme for shareholders) were presented as ways to refocus the group on its core Spanish operations without the integration risks inherent in the BBVA transaction.

The government’s stance and the complexity of the regulatory conditions were leveraged to argue that BBVA’s economic case was fragile, that synergies were delayed and uncertain, and that the exchange offer did not fairly compensate shareholders for assuming those risks.

Integration

Because the offer lapsed, BBVA’s integration plans remained at the level of projections and governance blueprints. They nonetheless reveal how the combined group was expected to be run and where value was sought.

Leadership and Governance

The transaction was consistently presented as a full integration, with BBVA as the surviving listed parent and Sabadell folded into its Spanish franchise over time. Public materials and investor presentations assumed continuity of BBVA’s top leadership (Executive Chair Carlos Torres Vila and CEO Onur Genç) and the absorption of Sabadell’s governance structures into BBVA’s own board and committee framework. However, BBVA emphasised that it intended to preserve Sabadell’s “best strengths,” including its SME expertise and regional franchises as Sabadell managers in those areas would be integrated into the combined Spanish business as segment or regional heads.

From a regulatory perspective, the Spanish government’s requirement that BBVA and Sabadell remain separate legal entities with autonomous management for at least three years would have forced a two‑stage governance model. In the first stage, each bank would keep its own board and senior management responsible for day‑to‑day operations, risk and compliance, while overarching strategy, capital allocation and synergy capture would be coordinated at BBVA‑group level. Only after the standstill period could a second‑stage legal merger proceed, collapsing the dual structure into a single corporate entity with unified governance.

People and Talent

According to an early statement, BBVA sought growth rather than cost-cutting, but the synergy case clearly contemplated rationalisation of overlapping functions. Sabadell’s board repeatedly warned shareholders that, notwithstanding these assurances, significant headcount reductions in branches and central services were a realistic outcome once the government’s separation condition expired. (see below)

BBVA’s offer materials noted that Sabadell shareholders would own roughly 17% of the enlarged BBVA after completion (on the improved terms). There is no public indication of bespoke retention packages beyond BBVA’s standard remuneration and long‑term incentive frameworks.

Synergies and Financial Projections

Facing investors, BBVA estimated annual pre‑tax synergies of around €900 million by 2029, representing about 14% of the combined Spanish cost base once Sabadell’s UK unit TSB is excluded. These savings were expected to derive mainly from consolidation of overlapping branches and business centres, integration of IT and digital platforms (BBVA’s proprietary

technology across Sabadell’s customer base), streamlining of corporate and support functions, and funding cost and capital efficiencies. BBVA argued that, once fully realised, these synergies could lift group earnings per share by roughly 20 to 25% versus a standalone scenario and support an additional €5 billion in annual lending to the Spanish economy.

Legal Representation and Advisory Footprint

Banco Sabadell engaged a consortium of global investment banks including Evercore, Goldman Sachs and Morgan Stanley as financial advisers to support its defence and valuation. On the legal side, Sabadell retained Cravath, Swaine & Moore LLP as U.S. counsel, a firm with practice in shareholder activism and defence, which publicly disclosed its role in advising the bank on the bid. For a Spanish bank defending against a Spanish bidder in a Spanish regulatory process, the engagement of a leading New York M&A defence firm signals that Sabadell anticipated the need for U.S. law shareholder communication strategy and SEC disclosure management alongside the Spanish process. It is worth noting because BBVA is listed on U.S. exchanges and filed Form 6-K and Form 425 materials with the SEC. BBVA was advised by UBS, Garrigues, and Linklaters, among others.

Legal Contentions & Regulatory Impact

Legal & Regulatory Issues

Overview of Authorities Involved:

Spanish National Securities Market Commission (CNMV) - approves the takeover prospectus, supervises the bid process, enforces takeover rules (Royal Decree 1066/2007 and the Spanish Securities Market Law).

Spanish National Markets and Competition Commission (CNMC) - reviews the acquisition under Spain’s Competition Act (Ley de Defensa de la Competencia), assessing horizontal and conglomerate effects in retail banking, deposits and lending.

Spanish Government / Council of Ministers (Ministry of Economy, Commerce and Business) - exercises sector‑specific powers over bank mergers and “economic concentrations” involving systemic institutions, including the power to impose public‑interest conditions even after CNMC clearance

European Commission, ECB, and EU framework - having ruled against the CMNV’s rejection of the bid, giving the green light to go on with the acquisition.

Key Issues and Concerns

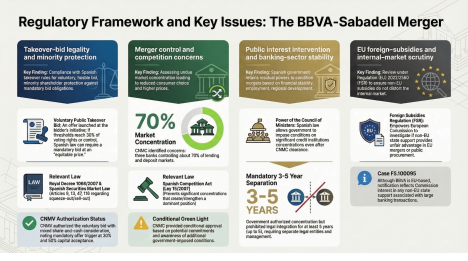

1. Takeover‑bid legality and minority protection

The first limb of the issue consisted of compliance with Spanish takeover‑bid rules for a voluntary, hostile bid, protection of minority shareholders, and potential mandatory bid obligation if BBVA crossed 30% but below control thresholds.

A voluntary public takeover bid is an offer launched at the bidder’s initiative for some or all shares of a listed company; if certain thresholds are crossed (typically 30% of voting rights or control), Spanish law can require a mandatory bid at an “equitable price” in cash or with a cash alternative.

Relevant law:

Royal Decree 1066/2007 on takeover bids (Articles 9, 13 and 47).

Spanish Securities Market Law (Ley del Mercado de Valores), including Article 116 on squeeze‑out and sell‑out mechanisms.

CNMV authorised BBVA’s voluntary bid, allowing a mixed share‑and‑cash consideration not subject to the “equitable price” test applicable to mandatory bids, while noting that a subsequent mandatory offer could be triggered if it reaches a level of acceptance of at least 30% and 50% of Sabadell’s capital.

The procedural history of BBVA's compliance with this framework was itself a significant source of delay and deal uncertainty. When BBVA first filed its takeover prospectus with the CNMV in late 2024, the CNMV declined to authorise it, a decision that was extraordinary in the context of Spanish M&A practice, where prospectus rejection at that stage is rare. The CNMV's refusal was grounded in concerns about the sufficiency of disclosure around the regulatory conditions and the adequacy of the consideration given the intervening share price movements of both banks since the initial announcement. BBVA challenged this decision and the European Commission intervened by issuing a letter in July 2025 questioning whether Spain's regulatory conduct, taken in aggregate across the CNMV, the CNMC, and the Council of Ministers, was compatible with EU rules on the free movement of capital. That intervention did not constitute a formal infringement proceeding, but it applied pressure on Spanish authorities and contributed to the CNMV's subsequent authorisation of the revised prospectus in September 2025. The CNMV's authorisation confirmed that BBVA's voluntary structure, with a share-for-share exchange consideration, was not subject to the equitable price test applicable to mandatory bids, and noted that a mandatory bid obligation would only crystallise if BBVA crossed 30% acceptance and subsequently sought control, a threshold it never reached. The acceptance period ran from 8 September to mid-October 2025, and with only approximately 25 to 26% of Sabadell's share capital tendered against a 50% minimum condition (not the 30% mandatory bid threshold) the offer lapsed automatically without triggering any mandatory follow-on obligation.

2. Merger control and competition concerns

Whether the combination would unduly concentrate the Spanish banking market, raising risks of reduced consumer choice and higher prices.

Merger control requires that significant concentrations be notified to the competition authority, which assesses whether the transaction may significantly impede effective competition, for example by leading to the creation or strengthening of a dominant position.

Relevant law:

Spanish Competition Act (Ley 15/2007, de Defensa de la Competencia).

Potentially Articles 101 and 102 TFEU in the background, through EU competition principles.

The CNMC’s review of BBVA-Sabadell identified concerns that the merger would leave roughly three banks controlling about 70% of lending and deposit markets, raising questions about dominance in certain regions and segments. While CNMC gave a conditional green light, it did so against a background of potential commitments (confidential in part) and with awareness that additional public interest conditions in relation to consumer rights, and fair market practice might be imposed by the government.

In practice, the merger control process was the longest and most structurally consequential regulatory phase of the entire transaction. The CNMC opened a Phase II investigation (reserved for concentrations raising serious competition concerns that cannot be resolved in the initial screening) in late 2024, committing the deal to an eleven month review before clearance was granted on 30 April 2025. Phase II involves a market investigation, a statement of objections setting out the authority's preliminary concerns, and a formal commitments procedure in which the parties negotiate remedies designed to address those concerns. The CNMC's key finding was that the combined BBVA-Sabadell entity would control approximately 70% of lending and deposit markets when aggregated across the three dominant institutions, and that the concentration of SME banking in specific regions, Catalonia and the Balearic Islands in particular, raised serious concerns about reduced competitive choice and the availability of credit to smaller businesses. The remedies extracted were, by the CNMC's own characterisation, unprecedented in scope for a Spanish banking transaction. They included: a prohibition on closing branches in municipalities with a population below 5,000 inhabitants; an obligation to maintain Sabadell's specialist SME offices as operationally distinct units; a requirement to preserve teller and in-person banking services; and a commitment to maintain aggregate SME credit volumes within specified ranges in the identified high-concentration geographies. These remedies were binding for a defined period and were structured to run alongside the government's separate integration prohibition: meaning that BBVA would have faced two overlapping sets of behavioural constraints simultaneously, one derived from competition law and one from public interest powers, each with its own enforcement mechanism and duration.

3. Public interest intervention and banking-sector stability

The Spanish government’s imposition of a three year minimum separation between BBVA and Sabadell, with possible extension to five years, as a condition for authorising the “economic concentration.”

In certain sectors, especially banking, governments retain residual powers to condition or influence mergers beyond pure competition law, based on financial stability, employment, regional development or consumer‑protection concerns.

Relevant framework:

Spanish banking and financial stability legislation that gives the Council of Ministers a say over concentrations involving significant credit institutions (interacting with Bank of Spain and ECB/SSM oversight).

General public‑interest doctrines recognised in Spanish law allowing the government to impose conditions when authorising concentrations already cleared by CNMC, particularly in critical infrastructures and financial institutions.

This power was exercised by authorising the concentration but prohibiting the legal integration of BBVA and Sabadell for at least three years, and possibly up to five, forcing them to operate as separate legal entities with independent assets and management during that period.

The mechanism by which the Spanish government intervened deserves close attention, because it is the element that most diverges from prior Spanish banking M&A practice and that generated the most sustained legal controversy. Under Spanish law, the Council of Ministers retains a residual power to impose conditions on concentrations involving significant credit institutions even after competition clearance has been granted by the CNMC: a power that operates separately from, and in addition to, the CNMC's own remedies regime. In BBVA-Sabadell, this power was exercised by a Council of Ministers resolution dated approximately eight weeks after the CNMC's own Phase II clearance. The resolution authorised economic concentration but imposed a prohibition on legal integration for a minimum of three years, extendable to five, requiring BBVA and Sabadell to maintain separate legal personalities, independent balance sheets, autonomous management structures, and distinct boards throughout that period. It is devastating for the synergy case. While the Commission did not formally prohibit the government's intervention, it signalled that using public interest powers to impose multi-year integration prohibitions on transactions that had received competition clearance was at the outer edge of what EU law permits, and that further escalation was possible if the Spanish framework were applied in a manner that constituted a disproportionate restriction on cross-border capital flows.

4. EU foreign‑subsidies and internal‑market scrutiny

Review under Regulation (EU) 2022/2560 on foreign subsidies distorting the internal market (the Foreign Subsidies Regulation, FSR).

The FSR empowers the European Commission to investigate whether non‑EU subsidies (or certain state supports) granted to companies can distort competition in EU mergers, public procurement or general market operations.

Relevant law:

Regulation (EU) 2022/2560 of 14 December 2022 on foreign subsidies distorting the internal market.

While BBVA is an EU‑based institution, the notification regards the Commission's interest in understanding any non‑EU state support or cross‑border distortions given the nature of its operations. The application of the FSR to BBVA-Sabadell was notable because BBVA is itself an EU-domiciled institution, which placed it in an unusual position relative to the FSR's primary design purpose. The regulation was conceived principally to address non-EU state-backed entities acquiring European companies with the advantage of foreign subsidy support that EU state aid rules cannot reach. BBVA's notification under the case showed the Commission's interest in understanding whether BBVA's extensive operations outside the EU, principally in Turkey and in Latin America, had benefited from forms of state support or preferential treatment from non-EU authorities that could constitute foreign subsidies within the FSR's scope. The Commission's clearance confirmed that no actionable foreign subsidies had been identified in the context of the transaction and that the FSR posed no obstacle to the bid proceeding. For practitioners, this notification lies less in its outcome than in its precedent: it established that large EU financial groups with material non-EU operations and governmental relationships in those markets will routinely face FSR notification obligations in future acquisitions of EU targets, regardless of whether the acquirer is EU-headquartered.

Industry Impact

The BBVA-Sabadell process represents a meaningful point in the regulatory treatment of domestic banking consolidation in Spain, and its significance can only be properly understood against the backdrop of what came before it.

The reference point is CaixaBank's acquisition of Bankia in 2020, the largest domestic banking merger Spain had seen and one that sailed through competition clearance with relative speed. The CaixaBank-Bankia deal was reviewed under a first-phase procedure, attracted remedies addressing localised branch concentration and financial exclusion risks in specific municipalities, and closed without a multi-year prohibition on legal integration or sustained intervention at the ministerial level. The political ‘temperature’ around that transaction was contained: it was framed as a necessary rationalisation of an oversupplied domestic market still carrying the structural wounds of the savings bank crisis, and the regulator treated it accordingly. BBVA-Sabadell could not have been more different. It ran through an eleven-month Phase II review before the CNMC, triggered a formal public consultation by the Ministry of Economy, produced what the CNMC itself characterised as unprecedented remedies in scope, and ultimately attracted additional conditions imposed directly by the Council of Ministers (a layer of governmental intervention that went beyond anything seen in the Bankia transaction and that prompted debate about the permissible limits of public interest review in banking M&A).

What explains the contrast? The answer lies in the changed market structure that the CaixaBank-Bankia deal itself produced. By 2024, Spanish retail banking was already significantly concentrated: CaixaBank and Santander together commanded a dominant share of the domestic deposit and lending market, with BBVA and Sabadell occupying the third and fourth positions respectively. A BBVA-Sabadell combination would not just have added scale; it would have created a second institution approaching parity with CaixaBank and materially reduced the number of meaningful competitors in the retail market to three. In that environment, the CNMC's Phase II concerns were structurally different from those that applied in 2020: the question was not whether a weakened savings bank should be absorbed to prevent disorderly failure, but whether a commercially motivated bid by a healthy acquirer should be permitted to compress competitive choice in a market already operating with limited rivalry. That is a harder case to clear, and the remedies reflect it.

The sensitivities of a retail-heavy market amplified every dimension of scrutiny. Spanish retail banking is not simply characterised by high branch density relative to other eurozone markets, it is a market in which the branch network remains genuinely material to credit access for SMEs, micro-enterprises, and private customers in non-metropolitan areas. The competitive dynamic in SME lending in particular depends on relationship proximity: unlike large corporate credit, which is priced and executed at the centre, SME lending in Spain is intermediated through local branch officers with regional book knowledge and direct client relationships. When business and professional groups warned that the merger could produce up to 10,500 job losses, close between 589 and 883 branches, and reduce SME credit availability by an estimated eight percent (equivalent to approximately €54 billion) they were articulating a concern that was both politically and analytically grounded. In regions like Catalonia and the Balearic Islands, where the combined BBVA-Sabadell share in SME banking would have been highest, the systemic dependency on those relationship networks was most acute, which is precisely why the CNMC's remedies were most granular in those geographies: commitments not to close branches in municipalities below 5,000 inhabitants, to maintain specialist Sabadell SME offices, to preserve teller services, and to hold aggregate SME credit volumes within a specified range for a defined period.

More broadly, the BBVA-Sabadell case reflects a hardening of national regulatory posture that sits in tension with the direction at European level. ECB supervisors and the European Commission have in recent years signalled clear support for scale-enhancing consolidation within the eurozone banking sector, on the grounds that European banks remain subscale relative to their US and Asian peers and that larger institutions are better positioned to absorb the investment costs of digitalisation and to provide competitive capital markets alternatives to corporates. The Banking Union framework was designed, in part, to facilitate cross-border and domestic combinations that would produce stronger, better-capitalised institutions. Against that, the BBVA-Sabadell outcome, in which a transaction that posed no threat to financial stability and would have created a well-capitalised group operating within ECB supervision was effectively frustrated by a combination of remedies, political conditions, and shareholder caution, sits as a case study in the gap that persists between European supervisory intent and national political reality. For future consolidators in retail-heavy eurozone markets, is a message may be implied? The more a deal touches branch networks, regional credit supply, and employment in electorally salient communities, the more likely it is that national authorities will use the tools available to them to shape or slow the transaction? even where formal prohibition is not warranted?

House View

The BBVA-Sabadell bid failed because it was the wrong vehicle for the right strategic idea, executed in the wrong way at the wrong moment in the political cycle. That is not a trivial distinction: the underlying logic of combining these two institutions was sound, and in a different configuration (a negotiated deal, offered at a credible premium, without the backdrop of post pandemic political sensitivity about employment and credit access), a BBVA-Sabadell merger might well have been both commercially defensible and regulatorily achievable. Perhaps the hostile structure was a generative cause of subsequent problems.

One consideration may be: A voluntary transaction, had Sabadell's board been brought to the table at a price that reflected fair value, would have changed the entire proceeding. A negotiated offer carries a recommendation; a recommended offer produces shareholder certainty; shareholder certainty removes the spectre of a lapsed bid and the one-year bar; and a board that is formally committed to the combination rather than actively defending against it is a profoundly different counterparty in competition and public interest proceedings. By choosing the hostile route (and by doing so with an initial offer that Sabadell's management immediately and credibly dismissed as undervalued) BBVA handed its opponents, from the Sabadell board to the Spanish government to the CNMC, a sustained period in which to organise resistance. The eleven-month Phase II review was, in significant part, a product of that hostile dynamic: it gave the government the temporal space to engage in consultation and to impose conditions, and it gave institutional shareholders the opportunity to watch the regulatory risk compound in real time and price it into their decision to hold rather than tender.

On the question of whether the deal would have succeeded had it been completed: the answer is likely that it would have faced structural issues regardless of the regulatory conditions, but that those conditions were not necessarily fatal to the long term strategic rationale. The €900 million synergy target (achievable in full only in 2029 after legal merger, with phased projections of €175 million in 2027 and €235 million in 2028) was not unrealistic for a transaction of this scale, but it was highly sensitive to execution risk in a market where integration history, including Sabadell's own experience with CAM and TSB, should have prompted caution. The CNMC conditions restricting branch closures and requiring maintenance of SME credit volumes in concentrated regions would have eroded the cost base of those synergies for several years; the separation requirement, in effect compelling BBVA and Sabadell to operate as independent institutions during the remedies period, would have created parallel cost structures that would have further compressed near-term returns. Had the deal closed at the offer price implied by BBVA's bid, it is difficult to construct a credible scenario in which the economics were compelling for a medium-term horizon. The deal was optimistically priced at a moment of uncertainty, and the subsequent layering of conditions would have made a previously marginal business case actively difficult to sustain.

The broader lessons are uncomfortable for deal makers and advisers in this sector. First, the hostile bid seems poorly suited to banking M&A in politically exposed retail markets, and BBVA's experience should be read as a structural and political constraint rather. Banking consolidation, more than almost any other sector, requires the consent of regulators, governments, and social partners, because banks are not merely commercial entities but providers of critical infrastructure. A bidder that chooses to bypass target board consent in that environment is effectively choosing to fight a multi-front war. Against the board, against the competition authority, against the government, and against an organised shareholder base that has been given every incentive to value the risks of tendering above the risks of remaining independent. The asymmetry extreme and the outcome here reflected it.

Second, the treatment of the synergy case by BBVA deserves scrutiny. The downward revision to synergy projections mid-process, from a headline of €900 million to disclosed phased figures of €175 million and €235 million for 2027 and 2028 respectively, was a substantive concession that the remedies imposed would materially delay the value creation argument. That revision should have been a signal to institutional shareholders that the gap between bid price and deliverable value was wider than the initial offer communicated, and it appears to have contributed materially to the low acceptance rate of approximately 26%. Shareholders were being rational. A bid that has been forced to revise its own value creation narrative downward mid-process, in a deal whose structure has been criticised from every political direction, is not a bid that warrants the risk of tendering ahead of a threatened lapse.

Finally, the outcome raises a question about the direction of European banking consolidation that does not have an easy answer. The European Commission and the ECB are right that scale matters: that the fragmented structure of eurozone retail banking imposes real costs on competitiveness, on digital investment capacity, and on the ability of European banks to allocate capital efficiently across the union. But the instruments available to achieve that consolidation at the national level are demonstrably inadequate in markets where governments retain robust public interest powers and where they are political issues. Until there is a more credible framework at the European level for managing the social transition costs of banking consolidation, one that does not leave national authorities as the sole arbiters of its implications, large-scale retail banking combinations within eurozone member states will continue to face the same cocktail of political resistance, indirect extended review, and shareholder caution that ultimately sank this deal.

References

Addleshaw Goddard. “The BBVA/Sabadell Case: Government Oversight and the Spanish Banking Merger.” July 15, 2025. https://www.addleshawgoddard.com/en/insights/insights-briefings/2025/competition/bbva-sabadell-case-government-oversight-spanish-banking-merger/

Banco Sabadell. Response to BBVA’s Hostile Tender Offer. https://comunicacion.grupbancsabadell.com/wp-content/uploads/Response-to-BBVAs-hostile-tender-offer.pdf

“Banco Sabadell’s Board Unanimously Recommends Shareholders Reject BBVA’s Takeover Bid.” January 18, 2026. https://comunicacion.grupbancsabadell.com/en/press-room/banco-sabadells-board-unanimously-recommends-shareholders-reject-bbvas-takeover-bid/

BBVA. 2024 Consolidated Annual Accounts and Management Report. February 10, 2025. https://shareholdersandinvestors.bbva.com/wp-content/uploads/2025/02/5_2_ENG_2024_Consolidated_Annual_Accounts_and_Management_Report.pdf

Annual Report 2024. February 27, 2025. https://shareholdersandinvestors.bbva.com/wp-content/uploads/2025/02/Informe-anual-2024_ENG.pdf

“The European Commission Completes Its Review of the BBVA and Banco Sabadell Transaction.” November 25, 2024. https://www.bbva.com/en/bbva-offer-sabadell/the-european-commission-completes-its-review-of-the-bbva-and-banco-sabadell-transaction/

“The Integration of BBVA and Sabadell Is a Transaction for Growth.” April 3, 2025. https://www.bbva.com/en/economy-and-finance/the-integration-of-bbva-and-sabadell-is-a-transaction-for-growth/

“CNMC Approves the Union of BBVA and Banco Sabadell Subject to Remedies to Ensure Financial Inclusion, Territorial Cohesion and Lending to SMEs and the Self-Employed.” April 30, 2025. https://shareholdersandinvestors.bbva.com/wp-content/uploads/2025/04/20250430_OIR_ENG.pdf

Inside Information Notice Regarding the Spanish Government’s Review of the Bid. May 27, 2025. https://shareholdersandinvestors.bbva.com/wp-content/uploads/2025/05/20250527_OIR_ENG-.pdf

“Banco Bilbao Vizcaya Argentaria, S.A. Announcement Regarding the Council of Ministers’ Decision on the BBVA/Sabadell Transaction.” June 23, 2025. https://shareholdersandinvestors.bbva.com/wp-content/uploads/2025/06/20250624_IP_ENG.pdf

“BBVA to Move Forward with the Transaction with Banco Sabadell.” June 30, 2025. https://shareholdersandinvestors.bbva.com/wp-content/uploads/2025/06/20250630_-IP_ENG.pdf

Prospectus of the Voluntary Takeover Bid of Banco de Sabadell (English translation). September 2, 2025.https://www.bbva.com/wp-content/uploads/2025/09/Prospectus-of-the-voluntary-takeover-bid-of-Banco-de-Sabadell-English-translation.pdf

“BBVA Increases Offer to Banco Sabadell Shareholders by 10% and Improves the Tax Treatment.” September 21, 2025. https://www.bbva.com/en/bbva-offer-sabadell/bbva-increases-offer-to-banco-sabadell-shareholders-by-10-and-improves-the-tax-treatment/

“Questions and Answers about the Offer to Banco Sabadell Shareholders.” October 9, 2025. https://www.bbva.com/en/bbva-offer-sabadell/questions-and-answers-about-the-offer-to-banco-sabadell-shareholders/

Bird & Bird. “CNMC Clears Bankia-CaixaBank Merger with Conditions.” April 17, 2021. https://www.twobirds.com/en/insights/2021/spain/cnmc-clears-bankia-caixabank-merger-with-conditions

Catalan News. “Spain Market Regulator Approves BBVA Takeover of Banc Sabadell.” September 5, 2025. https://www.catalannews.com/business/item/spain-market-regulator-approves-bbva-takeover-banc-sabadell-5-september-2025

CNBC. “Spain’s BBVA Announces $13 Billion Hostile Takeover Bid for Sabadell.” May 9, 2024. https://www.cnbc.com/2024/05/09/spains-bbva-announces-13-billion-hostile-takeover-bid-for-sabadell.html

CNMC (Comisión Nacional de los Mercados y la Competencia). Resolution Approving the BBVA/Sabadell Merger Subject to Commitments. April 30, 2025. https://www.cnmc.es/prensa/autorizacion-compromisos-bbva-sabadell-20250430

CNMV (Comisión Nacional del Mercado de Valores). Supplementary Report by the Board of Directors of Banco de Sabadell. https://www.cnmv.es/webservices/verdocumento/ver?t=%7B3bbfd17a-1d8b-4f1c-9db0-f179085d5c29%7D

“The CNMV Authorises the Voluntary Takeover Bid for the Shares of Banco Sabadell, S.A. Submitted by BBVA.” September 5, 2025. https://www.cnmv.es/webservices/verdocumento/ver?t=%7B96d25fac-f4b7-4349-9783-e4000227f512%7D

“Authorisation of the Modification of the Characteristics of the Voluntary Takeover Bid for Banco Sabadell.” September 25, 2025. https://www.cnmv.es/webservices/verdocumento/ver?t=%7Bf763ec70-c1ae-43b6-9a9a-ead5b3cec53d%7D

Cravath, Swaine & Moore LLP. “Banco Sabadell’s Defense Against BBVA’s Takeover Bid.” October 19, 2025. https://www.cravath.com/news-insights/banco-sabadells-defense-against-bbvas-takeover-bid.html

El País. “The Keys to BBVA’s Defeat in Its Takeover Bid for Sabadell.” October 17, 2025. https://english.elpais.com/economy-and-business/2025-10-17/the-keys-to-bbvas-defeat-in-its-takeover-bid-for-sabadell.html

Euronews. “BBVA Fails in €17bn Takeover Battle for Smaller Spanish Rival Sabadell.” October 17, 2025. https://www.euronews.com/business/2025/10/17/bbva-fails-in-17bn-takeover-battle-for-smaller-spanish-rival-sabadell

European Commission. FS.100095 — BBVA/Sabadell Foreign-Subsidy Review. November 2024.

Financial Times. “BBVA’s Bid for Sabadell.” October 2025. https://www.ft.com/content/9e2572d7-1254-4f09-b634-b53073cebf0c

MLex Market Insight. “BBVA Files Acquisition of Banco Sabadell Stake for EU Foreign Subsidy Review.” 2024–2025. https://www.mlexmarketinsight.com/news/insight/bbva-files-acquisition-of-banco-sabadell-stake-for-eu-foreign-subsidy-review

OTC Markets. Form 425 Filings Relating to BBVA’s Offer for Sabadell. 2025. https://www.otcmarkets.com/filing/html?id=18762659&guid=dKE-keIC06M4B3h

Retail Banker International. “EU Cautions Spain over Review of BBVA’s €11bn Sabadell Bid.” May 28, 2025. https://www.retailbankerinternational.com/news/eu-cautions-spain-bbva-sabadell-bid/

Reuters. “Spain’s BBVA Turns Hostile with $13 Billion Bid for Sabadell.” May 9, 2024. https://www.reuters.com/markets/deals/spains-bbva-announces-takeover-offer-sabadell-same-terms-2024-05-09/

“Spain’s Government Opposes BBVA’s $13 Billion Sabadell Hostile Bid.” May 9, 2024. https://www.reuters.com/markets/deals/spanish-government-opposes-bbvas-13-bln-sabadell-bid-2024-05-09/

“Spain’s Government Puts BBVA’s Bid for Sabadell Under Scrutiny.” May 27, 2025. https://www.reuters.com/sustainability/boards-policy-regulation/spanish-government-examine-bbvas-bid-sabadell-2025-05-27/

“Spain Says BBVA, Sabadell Cannot Integrate for at Least 3 Years.” June 24, 2025. https://www.reuters.com/sustainability/boards-policy-regulation/spanish-government-approves-bbva-bid-sabadell-with-conditions-2025-06-24/

“EU Challenges Spain for Hindering BBVA’s Sabadell Bid.” July 17, 2025. https://www.reuters.com/sustainability/boards-policy-regulation/eu-challenges-spain-hindering-bbvas-sabadell-bid-2025-07-17/

“BBVA Revising Synergy Estimates, Still Sees Value in Proposed Sabadell Deal.” August 7, 2025. https://www.reuters.com/business/finance/bbva-revising-synergy-estimates-still-sees-value-proposed-sabadell-deal-2025-08-07/

“BBVA Fails in $19 Billion Takeover Battle for Sabadell.” October 17, 2025. https://www.reuters.com/business/finance/bbva-fails-in-17bn-takeover-battle-for-smaller-spanish-rival-sabadell-2025-10-17/

S&P Global Market Intelligence. “Spanish Government Decision on BBVA Takeover of Sabadell Throws Deal into Question.” June 25, 2025. https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/6/spanish-government-decision-on-bbva-takeover-of-sabadell-throws-deal-into-question

Spain, Council of Ministers. Resolution Authorising the BBVA/Banco Sabadell Concentration Subject to Conditions. June 24, 2025.

United States Securities and Exchange Commission. BBVA Form 6-K Filing. 2025. https://www.sec.gov/Archives/edgar/data/842180/000119312525108558/d864309d6k.htm

BBVA No-Action Correspondence. September 2, 2025. https://www.sec.gov/files/corpfin/no-action/bbva-090225-incoming-letter.pdf