Pfizer’s $10 Billion Acquisition of Metsera

Deal Overview

Acquirer: Pfizer Inc.

Target: Metsera Inc.

Implied Equity Value: ~$9.2 billion (~7 billion cash upfront & up to ~$2.2 billion in contingent milestone payments)

Total Transaction Size: Up to $10 billion

Closing date: 13th November 2025

Target Advisor: Goldman Sachs & Co. LLC, Guggenheim Securities, Bofa Securities, Allen & Company LLC (Financial); Paul, Weiss, Rifkind, Wharton & Garrison LLP (Legal)

Acquirer Advisor: Citi (Financial); Wachtell, Lipton, Rosen & Katz (Legal)

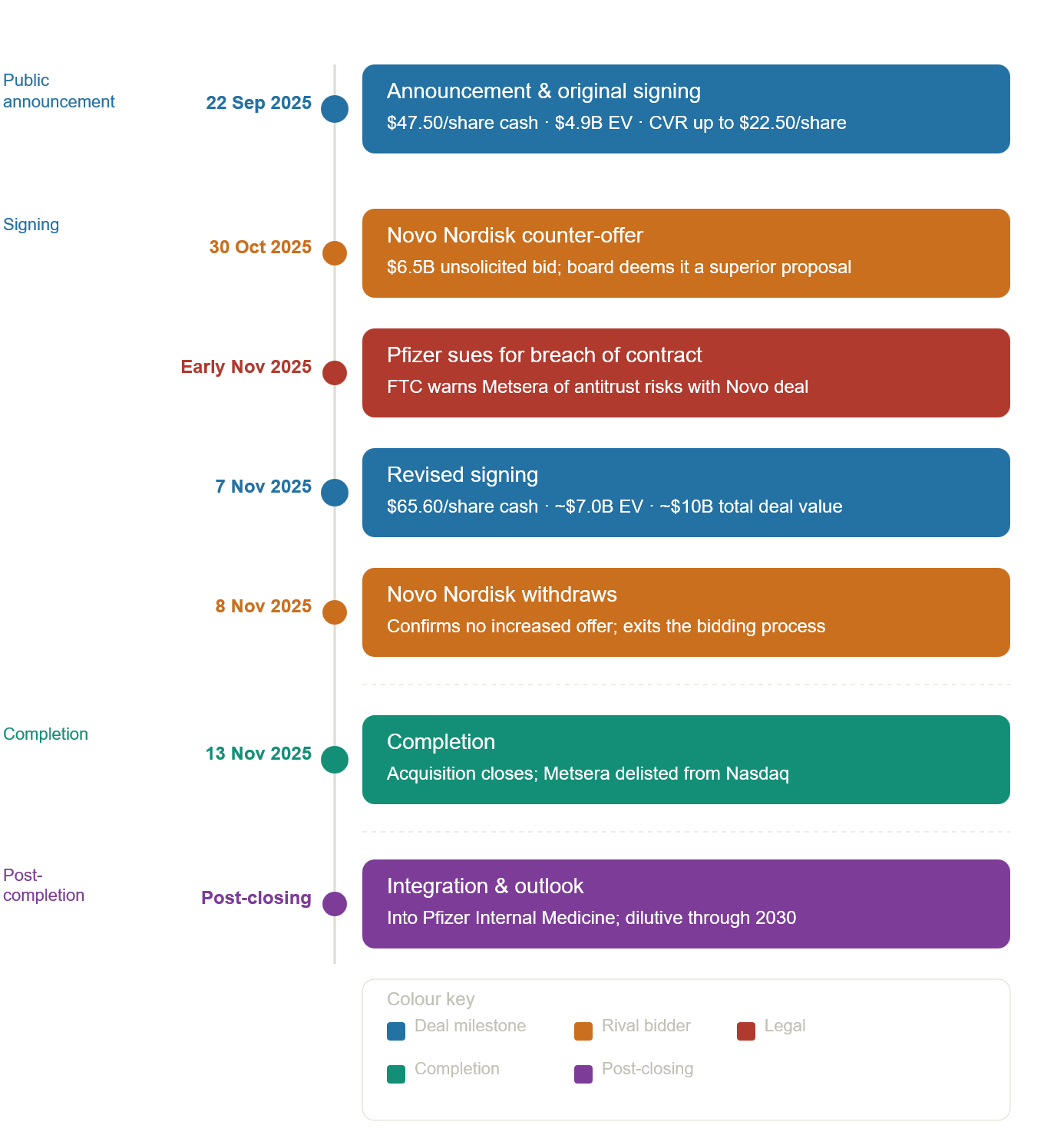

On 13th November 2025, Pfizer Inc. announced the successful completion of its $10 billion all‑cash acquisition of Metsera, a clinical-stage biopharmaceutical company accelerating the next generation of medicines for obesity and cardiometabolic diseases. Pfizer paid $65.60 per share in cash (~$7 billion enterprise value) plus a contingent value right of up to $20.65 per share tied to three clinical and regulatory milestones. This results in a potential total transaction value of up to $10 billion.

The deal followed a competitive bidding war between Pfizer and Novo Nordisk, after Novo submitted an unsolicited counterbid of up to ~$8.5 billion in late October. Pfizer filed a lawsuit alleging that Metsera and Novo Nordisk had breached the merger agreement and increased its total bid from ~$7.3 billion to ~$10 billion to match Novo’s increased bid of ~$10 billion. Given that Novo’s bid carried significant regulatory and antitrust risk, Metsera accepted Pfizer’s bid.

Strategically, this deal transforms Pfizer from a failed oral GLP-1 story to a broad obesity platform built around monthly injectables and oral combination therapies. This market is highly lucrative and competitive, estimated to reach a valuation of $100 billion by 2030. The transaction is expected to be dilutive through 2030, reflecting Pfizer’s commitment to further investment in several late-stage pipeline candidates.

“This strategic milestone represents more than a transaction — it is a deliberate investment in the future of medicine. By acquiring Metsera, we are directing our resources toward one of the most impactful and high-growth therapeutic areas and positioning ourselves to define it.”

Albert Bourla, Pfizer Chairman and Chief Executive Officer.

Company Details

Acquirer - Pfizer

Founded: 1849

Headquartered: New York, United States

CEO: Albert Bourla

Number of Employees: ~75,000

Market Cap*: $143.8bn

EV*: $189.7bn

LTM Revenue*: $62.8bn

LTM EBITDA*: $18.55bn

History & Background

Pfizer is a global biopharmaceutical company known for its strong research capabilities and broad innovation products across oncology, vaccines, immunology, and rare diseases. The company was founded in the mid-nineteenth century by two German immigrants who wanted to market a sweet-tasting remedy for intestinal parasites. Propelled by the need for medicines during the Civil War (1861–1865), the company was able to expand and branch out into industrial chemicals such as those used to make soft drinks. Pfizer then went public on June 22, 1942, listing on the New York Stock Exchange (NYSE) under the ticker PFE, offering 240,000 shares of common stock to the public in a $5.9 million initial public offering (IPO). The pharma giant has split its stock five times since its IPO.

During the early 1970s, Pfizer made a long-term investment in research. Recognising that the key to Pfizer's future growth lies in its ability to discover and develop innovative pharmaceuticals, Chairman Ed Pratt increased Pfizer’s Research & Development (R&D) budget from 5% - 15%, to 20% percent of sales. The company’s blockbuster era began during this period, surging through the 1990s and 2000s and driven by patent-protected hits such as Lipitor, Norvasc, Zoloft, Diflucan, Celebrex, and Prevnar.

Thanks to marketing such prescription drugs as Lipitor and Viagra, as well as over-the-counter medicines such as Centrum and Advil, Pfizer became one of the world’s largest pharmaceutical companies, with annual revenues of around $50 billion. Entering the 2020s, Pfizer developed one of the vaccines to fight COVID-19 in late 2020, and its annual revenue skyrocketed to $100.33 billion in 2022. Its COVID antiviral medication, Paxlovid, was approved by the Federal Drug Administration (FDA) the following year. On December 2, 2020, the Medicines & Healthcare Products Regulatory Agency (“MHRA”) in the U.K. granted temporary authorisation to Pfizer and BioNTech for emergency use for their COVID-19 mRNA vaccine (BNT162b2). This constituted the first Emergency Use Authorisation following a worldwide Phase 3 trial of a vaccine to help fight the pandemic. The vaccine, now called Comirnaty, became the first FDA-approved COVID-19 vaccine on Aug. 23, 2021.

Company Details (Target - Metsera)

Founded: 2022

Headquartered: New York, United States

CEO: Whit (Christopher) Bernard

Number of Employees: ~100-110

EV*: ~$7 billion

LTM Revenue*: $0 (pre-revenue)

LTM EBITDA: ($322.5m)

History & Background

Metsera is a clinical-stage biopharmaceutical company focused on developing next generation medicines for obesity and cardiometabolic diseases. Founded in 2022 with backing from ARCH Venture Partners and Population Health Partners, Metsera quickly assembled a portfolio of innovative incretin and amylin-based drug candidates aimed at safer, more effective weight loss. The company went public in January 2025, raising $275 million in an IPO at $18 per share. Although Metsera remains pre-revenue, with no marketed products to date, it secured a multi-billion-dollar acquisition price due to the significant market potential of its drug candidates.

Metsera publicly emerged from stealth in April 2024 and raised $290 million in Series B financing led by ARCH Venture Partners with participation from other leading healthcare investors such as F-Prime Capital, GV, Mubadala Capital, Newpath Partners and SoftBank Vision Fund 2, and other undisclosed investors. The investors envisaged a biotech that could offer the next generation in obesity care, covering issues that the leading approved medicines, Novo’s Wegovy and Lilly’s Zepbound, did not address. In September 2024, the Phase I trial of MET-097 showed a 7.5% reduction in body weight at day 36. Seven months later, Metsera raised another $215 million in a Series B financing led by Wellington Management and Venrock Healthcare Capital Partners to further advance its portfolio of highly differentiated, clinical-stage, Nutrient-Stimulated Hormone (NuSH) analog peptides. Metsera has raised over $500 million to date.

Metsera is advancing a suite of peptide and peptide-antibody conjugate drugs for weight loss and other indications, all based on GLP-1 agonists. The technical foundation for its drugs comes from Zihipp Limited, a London start-up Metsera acquired for its vast library of 20,000-plus gut hormone peptides. Zihipp was chaired by Stephen Bloom, who was among the first scientists to publish on the role of GLP-1 in appetite and now heads research and development at Metsera.

“Metsera’s portfolio is focused beyond the current generation of market leaders to address the full spectrum of future weight loss therapeutic needs, including effective weight maintenance, preserving muscle, less-frequent dosing, and better efficacy, tolerability and patient access.”

Kristina Burow, Metsera board member and Managing Director at ARCH Venture Partners.

The Acquisition

Pfizer’s binding all‑cash offer initially valued Metsera at approximately $4.9 billion, before a competing proposal from Novo Nordisk materially increased the transaction value. Pfizer ultimately agreed to acquire Metsera for up to $86.25 per share – more than $10 billion in aggregate – inclusive of CVRs.

To fund the consideration, Pfizer used a mix of newly issued senior unsecured notes and existing cash liquidity, including a $6 billion senior unsecured note offering priced in November 2025. The company entered closing with gross leverage of roughly 2.7x, as disclosed on its Q3 earnings call, and the Metsera cash outlay is set to lift this modestly above its near‑term target. Rating agencies assigned the new notes A‑category ratings with a stable outlook, signalling limited concern about a temporary increase in net debt‑to‑EBITDA.

The transaction consideration consists entirely of cash and CVRs, meaning Pfizer will not issue new equity or alter its existing share count. Nevertheless, the incremental interest expense associated with the cash financing, combined with increased R&D investment in Metsera’s pipeline, is expected to render the transaction earnings-dilutive for several years, primarily to enable further investment in several promising late-stage pipeline candidates.

Timeline

Motivation

For Pfizer

This transaction brings together Pfizer’s global infrastructure with Metsera’s next generation obesity portfolio, particularly its lead pipeline asset, MET-097i, a GLP-1 receptor agonist designed for once-monthly injection. MET-097i fills a critical gap in Pfizer’s pipeline, as the company had no competitive late-stage obesity asset.

Re-entering the obesity and cardiometabolic market: Pfizer’s acquisition of Metsera represents a high-stakes move to rebuild its long-term growth engine by securing differentiated, late-stage obesity assets, specifically PF-3944 and PF-3945. Facing intense pressure to demonstrate a renewed commitment to a market now central to chronic disease management, Pfizer used the acquisition to bolster its competitive standing. This shift serves as a vital strategic pivot following significant setbacks in its internal pipeline: with the 2023 discontinuation of lotiglipron and the early 2025 termination of danuglipron, Pfizer had been left without an internally developed oral GLP-1 programme.

Acquiring a scalable peptide innovation platform:

Metsera’s strength extends beyond MET‑097i to the proprietary peptide‑engineering platforms, which enable the rapid generation of differentiated incretin and non‑incretin therapies. These include:

MINT™ – A peptide engineering library of ~20,000 nutrient-stimulated hormone analogs, enabling the rapid generation of differentiated molecules.

HALO™ – A peptide lipidation and half-life extension technology that maintains peptide activity for over two weeks, facilitating monthly dosing schedules.

MOMENTUM™ – An oral delivery system achieving over five-fold higher bioavailability than oral semaglutide, designed to enable scalable oral GLP-1 therapies.

“Our team has invented and developed multiple injectable and oral candidate medicines and a category-leading peptide engineering platform, which together promise class-leading performance in a major sector of population health.”

— Whit Bernard, Co-founder and CEO of Metsera

Metsera’s proprietary engineering offers superior manufacturability and bioavailability, providing the cost-efficiency necessary to scale obesity therapies across diverse global markets. These platforms give Pfizer optionality beyond MET-097i: a monthly amylin analog (MET-233i), oral GLP-1 candidates (MET-097o, MET-224o), and a prodrug version of MET-097i for quarterly dosing (MET-815). In a market where adherence and convenience dictate success, owning these platforms enable Pfizer to develop a continuous stream of in‑house candidates.

Diversification of products:Pfizer has established a new therapeutic pillar in chronic weight management by securing the following clinical-stage assets:

PF-3944 / MET-097i — an ultra-long-acting GLP-1 currently in Phase III trials for chronic weight management, administered weekly or once-monthly; and

PF-3945 / MET-233i — an ultra-long-acting amylin analog in Phase I/II trials, being developed in combination with PF-3944 as a GLP-1–amylin combination for chronic weight management.

With these additions, Pfizer now possesses a multi-modality obesity pipeline. This diversified portfolio targets the GLP-1 receptor, glucose-dependent insulinotropic polypeptide receptor (GIPR) agonists and antagonists, and amylin analogs across both injectable and oral delivery formats.

Pfizer’s Product Pipeline

Pfizer’s marketed portfolio encompasses the full spectrum of modern therapeutics, maintaining established and emerging brands across prevention, treatment, and specialty care. In 2024, the company reported $63.6 billion in revenue and has since prioritised "tighter execution" across key products and geographic regions.

Vaccines

Prevnar 20 – Vaccine to prevent pneumonia.

Abrysvo (RSV) – Vaccine to prevent lower respiratory tract disease (LRTD).

Comirnaty (COVID-19 mRNA) – Vaccine to prevent COVID-19.

Internal Medicine (cardio-metabolic / neuroscience)

Eliquis (apixaban) – Oral anticoagulant that reduces the risk of stroke, pulmonary embolism, and deep vein thrombosis.

Vyndaqel / Vyndamax (tafamidis) – Transthyretin (TTR) stabilisers slowing down the formation of amyloid deposits that cause heart damage.

Nurtec ODT / Vydura (rimegepant) – CGRP receptor antagonist indicated for both the acute treatment and prevention of episodic migraine.

Oncology (incl. legacy Seagen brands)

Ibrance (palbociclib) – CDK4/6 inhibitor that blocks cancer cell replication in HR-positive, HER2-negative breast cancer.

Xtandi (enzalutamide) – Androgen receptor inhibitor used in the treatment of prostate cancer.

Padcev (enfortumab vedotin) – A medicine used to treat adults with bladder cancer and cancers of the urinary tract.

Lorbrena (lorlatinib) – A third-generation, targeted kinase inhibitor used to treat adults with ALK-positive metastatic non-small cell lung cancer (NSCLC).

Anti-infectives & Hospital

Paxlovid (nirmatrelvir/ritonavir) – Oral treatment for COVID-19 in high-risk patients.

Zosyn (piperacillin/tazobactam) – A broad-spectrum antibiotic for severe hospital-acquired infections.

Zyvox (linezolid) – An antibiotic for serious Gram-positive infections, including resistant strains such as MRSA.

Inflammation & Immunology / Dermatology

Xeljanz (tofacitinib) – An oral JAK‑inhibitor immunosuppressant that reduces inflammation in autoimmune diseases.

Cibinqo (abrocitinib) – An oral JAK1 inhibitor used to treat moderate-to-severe atopic dermatitis (eczema).

Eucrisa (crisaborole) – A steroid-free topical ointment used to treat mild-to-moderate eczema.

For Metsera

Accelerating development of a high-potential pipeline: Operating as a clinical-stage company, Metsera faced significant hurdles in self-funding its high-potential pipeline and managing the complex operational demands of global Phase 3 trials. By integrating with Pfizer, Metsera gains immediate access to the requisite capital and global infrastructure necessary to accelerate its lead assets. This partnership significantly compresses the timeline for transitioning MET-097i into pivotal Phase 3 trials and navigating the global regulatory landscape.

De-risking clinical and commercial execution: The shift to late‑stage trials, global regulation, and commercial scale‑up is capital‑intensive and operationally demanding. Under Pfizer, Metsera is insulated from funding constraints and market volatility, leveraging Pfizer’s balance sheet and infrastructure to reduce both clinical‑execution and commercialisation risk.

Maximising platform potential across indications: Metsera’s proprietary engineering platforms—including MINT™, HALO™, and MOMENTUM™—possess broad utility beyond weight management. Pfizer’s multi-disciplinary expertise allows for the exploration of these platforms in adjacent metabolic and cardiovascular indications, such as Type 2 diabetes and MASH (metabolic dysfunction-associated steatohepatitis), which Metsera could not have pursued independently at the same scale.

Metsera’s Product Pipeline

Metsera’s pipeline centres on two candidates: MET-097i, a once-monthly GLP-1 injectable, and MET-233i, an injectable amylin analogue designed both as a monotherapy and as a co-formulated combination therapy with MET-097i in solution. According to David Risinger, analyst at Leerink Partners, “Metsera’s experimental obesity drugs, MET-097i, and MET-233i are projected to reach $5 billion in combined peak sales.” By targeting both injectable and oral modalities, Metsera aims to position itself across multiple segments of the rapidly expanding obesity market.

Injectable Incretin and Non‑Incretin Therapies (Core Growth Driver)

MET-097i (Lead Programme): An ultra‑long‑acting injectable GLP‑1 receptor agonist engineered for once‑monthly dosing. Phase 1b data indicate up to ~14% placebo‑adjusted weight loss at 28 weeks, positioning the asset as a differentiated alternative to weekly GLP‑1 therapies such as semaglutide and tirzepatide. The program is designed to compete on convenience, adherence, and durability of effect, all of which are increasingly important in chronic obesity management.

Combination Therapies (MET-097i + MET-233i): An early‑stage, ultra‑long‑acting injectable amylin analogue intended for monthly administration. It is being evaluated both as a monotherapy and in combination with MET‑097i, targeting complementary mechanisms to enhance weight‑loss efficacy, particularly for patients who respond poorly to GLP-1 therapies.

Oral GLP‑1 Therapies (Long‑Term Optionality)

MET-002: A predecessor peptide to MET-224, currently being assessed in Phase 1 as a prototype to identify an optimal clinical formulation for MET-224o / MET-097. While still in early development, the oral platform aims to achieve greater efficacy than existing small‑molecule oral GLP‑1s while improving patient preference and the potential to broaden access to obesity treatment.

Integration

Challenges for Pfizer

Leadership and governance alignment: Integrating Metsera’s scientific leadership and platform‑governance structures into Pfizer’s Internal Medicine and obesity division presents a material challenge, particularly given Pfizer’s recent setbacks with lotiglipron and danuglipron. Clear governance around clinical strategy, regulatory engagement, and platform development will be essential to avoid repeating prior execution failures.

Retention of key talent and platform expertise: Metsera’s value is concentrated in its scientific teams and proprietary peptide‑engineering platforms. Pfizer must retain core researchers, programme leads, and platform architects to preserve continuity across MET‑097i, MET‑233i, and the oral GLP‑1 programmes. Any loss of key personnel would weaken the scientific rationale for the acquisition and slow integration.

Challenges for Metsera

Clinical development risk: Metsera’s core assets are largely in Phase 2 development, with the company actively advancing its lead injectable GLP-1 candidate (MET-097i) through mid-stage trials toward Phase 3. Historical precedent highlights this risk, for example: Roche’s aleglitazar programme was terminated in Phase III after unexpected safety signals emerged, wiping out what had been viewed as a highly promising metabolic asset. This underscores that promising mid‑stage efficacy often fails to translate into superior pivotal‑trial outcomes. A late‑stage clinical failure would materially erode the acquisition’s long‑term value and negate the projected revenue synergies.

Financial and capital structure risk: The finalised terms require an upfront cash payment of $65.60 per share, valuing Metsera at up to $7 billion. This represents a substantial, non‑refundable capital commitment by Pfizer and places additional pressure on the balance sheet when Pfizer is operating close to its stated gross‑leverage threshold of approximately 2.7× and carries around $37.7 billion in current liabilities. Metsera’s development plans therefore depend on Pfizer’s ability to sustain investment without compromising broader capital‑allocation priorities.

Earnings dilution and long-term commercial risk: Pfizer forecasts around $0.16 of EPS dilution in 2026 and expects the deal to remain earnings‑dilutive throughout the decade as Metsera’s assets progress toward commercialisation. The company frames this as a strategic investment, noting that Metsera’s GLP‑1 and amylin programmes have the potential to deliver more than $5 billion in combined peak sales and to support Pfizer’s growth trajectory into the 2030s. Although the financing is expected to push leverage above Pfizer’s 2.7× target, management maintains that operating cash flow will enable a gradual return to its preferred capital structure while sustaining dividend commitments and broader capital‑allocation priorities. In its communications to investors, Pfizer emphasises that the temporary earnings drag does not alter its long‑standing commitment to shareholder returns.

Legal Contentions & Regulatory Impact

For context,a U.S. M&A bidding process typically involves the target running a structured auction, inviting selected buyers to submit indicative offers before granting a shortlist due diligence access and final bid rights. The board then negotiates with its preferred bidder and signs a merger agreement, after which any competing bids are subject to the contractual terms agreed with the original buyer.

The central antitrust concern was Novo Nordisk’s existing market power. Novo Nordisk is a leading global healthcare company, founded in 1923 and headquartered in Denmark. On October 31st, Pfizer Inc, in response to Novo’s unsolicited proposal, Pfizer filed its first lawsuit in the Delaware Court of the Chancery against Metsera, its board, and Novo claiming breach of contract, breach of fiduciary duty, and tortious interference and seeking a preliminary injunction. The court ultimately denied Pfizer’s motion for a preliminary injunction.

In conjunction with its contractual claims, Pfizer filed a second lawsuit against Metsera, its board, and Novo in the District of Delaware. In its complaint, Pfizer alleged that Novo, who has a 50% market share of GLP-1s, offered a $6.5 billion payment to Metsera, to protect its dominant position. The structure of the payment was purportedly designed to avoid initial antitrust regulatory review, as it would allow Metsera to “immediately and permanently dividend that cash to its shareholders” before reporting the transaction. The complaint goes on to allege that the defendants knew that Novo’s “dominant market position” in GLP-1s likely meant the merger would be blocked, but they did not “care.”

Pfizer alleged that the defendants’ payout agreement violated Section 1 and Section 2 of the Sherman Act and Section 7 of the Clayton Act, asserting both concerted action and monopolisation theories and that the proposed transaction risked substantially lessening competition in the GLP-1 market. The complaint further alleged that the deal mechanics were designed to front-load cash to Metsera shareholders and to blunt Hart-Scott-Rodino (HSR) scrutiny, conduct that would also implicate HSR filing obligations. Simultaneous with the Delaware filing, the FTC sent letters to Novo and Metsera raising concerns that the structure may have violated pre-merger notification requirements under the HSR Act. Days later, Pfizer increased its offer, Metsera’s board cited the FTC inquiry and the “unacceptably high legal and regulatory risks” of the Novo proposal, and Metsera agreed to a revised transaction with Pfizer.

Pfizer's acquisition of Metsera moved through regulatory clearance with limited friction. Metsera shareholders approved Pfizer’s revised cash‑and‑CVR offer on 13 November 2025 following a unanimous board recommendation, enabling the deal to close shortly thereafter. U.S. antitrust scrutiny proved modest: the Federal Trade Commission (FTC) granted early termination of the HSR waiting period for the transaction, signalling no substantive competition concerns in the obesity‑drug pipeline, even as the agency separately warned that Novo Nordisk’s rival bid carried “unacceptably high” regulatory risks for the GLP‑1 market. The more material legal tension arose from Pfizer’s contract and antitrust litigation against Metsera and Novo during the bidding contest; although the Delaware Court of Chancery declined to issue a temporary restraining order, the proceedings did not impede the shareholder vote or delay closing.

Industry Impact

Pfizer’s ability to differentiate Metsera’s assets could be constrained by the speed and intensity of rival innovation. The obesity pipeline is evolving faster than any single candidate can keep pace with, and Metsera's MET-097i (a GLP-1 mono-agonist) produced 14.1% placebo-adjusted weight loss at 28 weeks. Eli Lilly's retatrutide, a triple GIP/GLP-1/glucagon agonist, has produced up to 28.7% weight loss at 68 weeks in Phase 3, setting a new efficacy ceiling, while Novo Nordisk's amycretin, a dual GLP-1/amylin agonist, has delivered 22.0% weight loss at 36 weeks Pfizer with Phase 3 now underway. By the time MET-097i reaches market, both will be established benchmarks.

Metsera’s key point of differentiation, once-monthly injectable dosing, also faces pressure. Eli Lilly's orforglipron, a once-daily oral GLP-1 pill, produced comparable weight loss of up to 14.7% at 36 weeks without injection or dietary restrictions Pfizer, with regulatory submissions already in train. For patients achieving similar results with a daily pill, the value of a monthly injectable diminishes considerably.

On combination strategy, Metsera faces well-resourced competition on its own turf. Novo Nordisk is advancing amycretin in-house, while Roche moved swiftly into the amylin space via a 2025 licensing deal with Zealand Pharma for petrelintide. Phase 2 data showed Roche's petrelintide achieving up to 10.7% weight reduction at 42 weeks against just 1.7% for placebo, with tolerability indistinguishable from placebo Business Wire — a combination-ready asset landing squarely in Metsera's intended niche.

House View

Viewpoint

This deal gives Pfizer a credible point of differentiation in a market dominated by Eli Lilly and Novo Nordisk. While the final consideration reflects a meaningful premium to Metsera’s standalone fundamentals, the purchase aligns with Pfizer’s strategic imperative to rebuild its cardiometabolic pipeline and secure early exposure to the rapidly expanding obesity therapeutics market.

Emerging Risks

Market competition: The rapid pace of next‑generation and oral obesity treatments may diminish Metsera’s differentiation by the time of commercial launch.

Efficacy benchmarking: Higher‑efficacy triple/dual agonists from competitors could reset the clinical standard, compressing MET‑097i’s market and forcing price concessions. Securing head‑to‑head or combination data quickly is essential to defend value and label scope for Pfizer.

Overall, Pfizer’s acquisition of Metsera reflects a willingness to pay a meaningful premium for early access to scarce obesity innovation and long‑term optionality. While the price elevates execution risk, the strategic rationale is clear: patent expiries, the scale of the obesity opportunity, and rapidly shifting cardiometabolic dynamics justify an aggressive, optionality‑driven approach. The transaction’s success will hinge on Pfizer’s ability to accelerate Metsera’s clinical programme while preserving the biotech’s high‑science culture and innovation momentum.

References

Eli Lilly and Company (2025). Lilly's oral GLP-1, orforglipron, demonstrated statistically significant efficacy results and a safety profile consistent with injectable GLP-1 medicines in successful Phase 3 trial. [online]. Available at: https://investor.lilly.com/news-releases/news-release-details/lillys-oral-glp-1-orforglipron-demonstrated-statistically

Eli Lilly and Company (2025). Lilly's triple agonist, retatrutide, delivered weight loss of up to an average of 71.2 lbs along with substantial relief from osteoarthritis pain in first successful Phase 3 trial. [online]. Available at: https://investor.lilly.com/news-releases/news-release-details/lillys-triple-agonist-retatrutide-delivered-weight-loss-average

Metsera (2024). Metsera Launches to Lead the Next Generation of Medicines for Obesity and Metabolic Diseases. [online]. Available at: https://investors.metsera.com/news-releases/news-release-details/metsera-launches-lead-next-generation-medicines-obesity-and

Metsera (2024). Metsera Secures $215 Million Series B Financing to Further Accelerate Portfolio. [online]. Available at: https://investors.metsera.com/news-releases/news-release-details/metsera-secures-215-million-series-b-financing-further

Metsera (2025). Metsera Announces Pricing of Initial Public Offering. [online]. Available at: https://investors.metsera.com/news-releases/news-release-details/metsera-announces-pricing-initial-public-offering

Novo Nordisk (2025). Novo Nordisk successfully completes phase 1b/2a trial with subcutaneous amycretin in people with overweight or obesity. [online]. Available at: https://www.novonordisk.com/news-and-media/news-and-ir-materials/news-details.html?id=915251

Novo Nordisk (2025). Novo Nordisk ramps up obesity fight, advances amycretin to Phase III. [online]. Available at: https://www.clinicaltrialsarena.com/news/novo-nordisk-obesity-drug-phase-iii-trial-advance/

Pfizer (2025). Pfizer Enters into Definitive Agreement to Acquire Metsera. [online]. Available at: https://www.pfizer.com/news/press-release/press-release-detail/pfizer-enters-definitive-agreement-acquire-metsera

Pfizer (2025). Pfizer Files Federal Antitrust Claims in Second Lawsuit Against Metsera, its Controlling Stockholders and Novo Nordisk. [online]. Available at: https://www.pfizer.com/news/press-release/press-release-detail/pfizer-files-federal-antitrust-claims-second-lawsuit

Pfizer (2025). Pfizer Receives Early Clearance from U.S. Federal Trade Commission for Metsera Acquisition. [online]. Available at: https://www.pfizer.com/news/press-release/press-release-detail/pfizer-receives-early-clearance-us-federal-trade-commission

Pfizer (2025). Pfizer Responds to Delaware Chancery Court Ruling. [online]. Available at: https://www.pfizer.com/news/press-release/press-release-detail/pfizer-responds-delaware-chancery-court-ruling

Pfizer (2025). Pfizer Completes Acquisition of Metsera. [online]. Available at: https://www.pfizer.com/news/press-release/press-release-detail/pfizer-completes-acquisition-metsera

Pittock, H. (2025). Novo Nordisk's Offer To Acquire Metsera Constitutes Attempted Monopolization. ProMarket. [online]. Available at: https://www.promarket.org/2025/11/17/novo-nordisks-offer-to-acquire-metsera-constitutes-attempted-monopolization/

Roche (2025). Roche enters into an exclusive collaboration & licensing agreement with Zealand Pharma to co-develop and co-commercialise petrelintide as a potential foundational therapy for people with overweight and obesity. [online]. Available at: https://www.roche.com/media/releases/med-cor-2025-03-12

Roche (2026). Roche announces positive Phase II results for petrelintide, an amylin analog developed for people living with overweight and obesity. [online]. Available at: https://www.roche.com/media/releases/med-cor-2026-03-05

Shinder Cantor Lerner LLP (2025). Slimming Down A Monopoly – Pfizer Files Antitrust Lawsuit to Prevent an Acquisition. [online]. Available at: https://scl-llp.com/slimming-down-a-monopoly-pfizer-files-antitrust-lawsuit-to-prevent-an-acquisition/

Steuer, M. (2025). Novo Nordisk's Killer Non-Acquisition Merger Contract Proposal Is a Case of "Heads I Win, Tails You Lose". ProMarket. [online]. Available at: https://www.promarket.org/2025/11/11/novo-nordisks-killer-non-acquisition-merger-contract-proposal-is-a-case-of-heads-i-win-tails-you-lose/

Zealand Pharma (2025). Zealand Pharma and Roche enter collaboration and license agreement to co-develop and co-commercialize petrelintide as a future foundational therapy for people with overweight and obesity. [online]. Available at: https://www.globenewswire.com/news-release/2025/03/12/3041113/0/en/Zealand-Pharma-and-Roche-enter-collaboration-and-license-agreement-to-co-develop-and-co-commercialize-petrelintide-as-a-future-foundational-therapy-for-people-with-overweight-and-o.html

Zealand Pharma (2026). Zealand Pharma announces positive Phase 2 results for petrelintide, an amylin analog with potential to redefine the weight management experience for people living with overweight and obesity. [online]. Available at: https://www.globenewswire.com/news-release/2026/03/05/3250569/0/en/Zealand-Pharma-announces-positive-Phase-2-results-for-petrelintide-an-amylin-analog-with-potential-to-redefine-the-weight-management-experience-for-people-living-with-overweight-an.html